Pakistan is facing yet another challenge in the form of the recent arrest of former Prime Minister Imran Khan and the subsequent nationwide protests by his supporters. This development is a significant blow to the already struggling economy. Ironically, the arrest came a few days after China's Foreign Minister urged Pakistan to address its political instability to promote economic development. The economic crisis in Pakistan is characterized by a shortage of foreign reserves, inflation rates exceeding 36%, and a delayed IMF bailout, all of which are contributing to the country's destabilization.

The country’s total exports and remittances declined by 20% YoY and 11% YoY, respectively in March 2023. However, for the first nine months of FY23, Pakistan's current account deficit decreased by 74% to $3.4 billion, compared to $13.0 billion during the same period last year on back a substantial 36% YoY decrease in total imports.

According to recent results released by the Pakistani finance ministry, the country's total revenue stood at Rs 6.9 trillion, with tax revenue contributing Rs 5.6 trillion and non-tax revenue contributing Rs 1.3 trillion. Total expenditure was Rs 10 trillion, resulting in a massive budget deficit of approximately Rs 3.1 trillion. The government financed the budget deficit with around Rs 3.8 trillion in domestic borrowing. Additionally, the Pakistani government has paid Rs 3.1 trillion in domestic debt servicing, which accounts for 87% of the total debt servicing.

Read More: Recent Fiscal Results Underscore Urgency Of Domestic Debt Restructuring For Pakistan

Source: ARHL

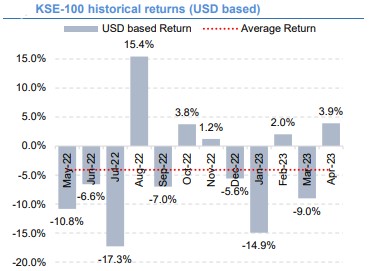

Investors' confidence in Pakistan is also low, with the Pakistan Stock Exchange (PSX) having one of its worst-performing years in 2022, and the current year has not been great either. Recent events are likely to further dent the PSX's performance.

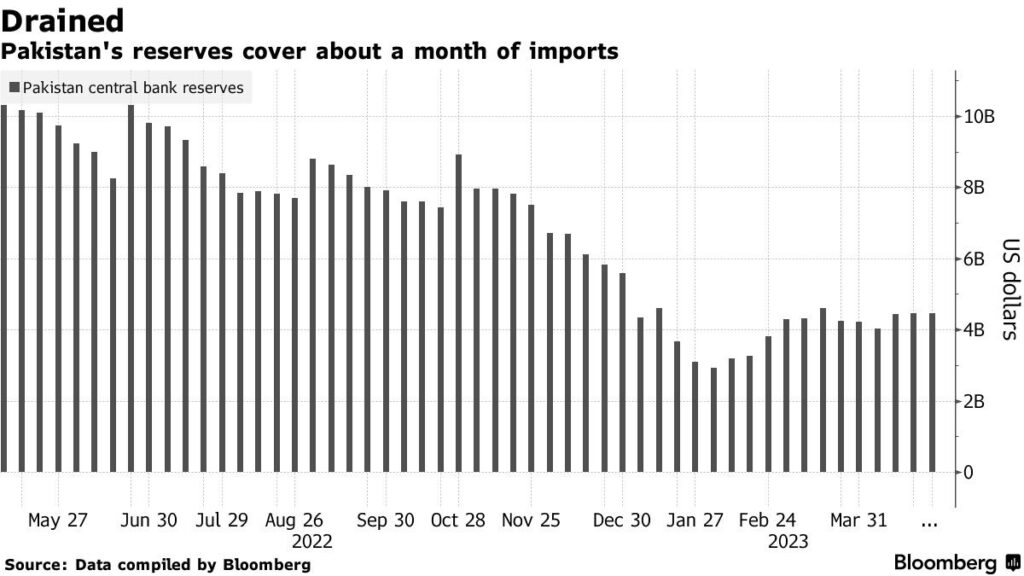

Meanwhile, the country is facing a challenging time in resuming the $6.5 billion bailout program from the IMF. The program has stalled due to the government's inability to meet certain loan conditions. Political tensions ahead of the upcoming elections add to the risk of a delay in the loan. The former premier’s arrest will only worsen the situation. The country is seeking to engage with the IMF beyond June, to secure additional financing from other multilateral and bilateral partners, which could reduce default risk. Pakistan's gross external financing needs are estimated to increase to 139.5% in fiscal year 2024, up from 133% in 2023.

Despite the historic low in civil-military relations, the immediate concern in Pakistan is the risk of default. Moody's ratings agency has already issued a warning, which should prompt those in power to take action. However, the chances of a deal seem low due to a lack of cohesion. Further, the arrest of Khan could exacerbate the situation, potentially leading to an economic meltdown in the country.

The country’s total exports and remittances declined by 20% YoY and 11% YoY, respectively in March 2023. However, for the first nine months of FY23, Pakistan's current account deficit decreased by 74% to $3.4 billion, compared to $13.0 billion during the same period last year on back a substantial 36% YoY decrease in total imports.

According to recent results released by the Pakistani finance ministry, the country's total revenue stood at Rs 6.9 trillion, with tax revenue contributing Rs 5.6 trillion and non-tax revenue contributing Rs 1.3 trillion. Total expenditure was Rs 10 trillion, resulting in a massive budget deficit of approximately Rs 3.1 trillion. The government financed the budget deficit with around Rs 3.8 trillion in domestic borrowing. Additionally, the Pakistani government has paid Rs 3.1 trillion in domestic debt servicing, which accounts for 87% of the total debt servicing.

Read More: Recent Fiscal Results Underscore Urgency Of Domestic Debt Restructuring For Pakistan

Source: ARHL

Investors' confidence in Pakistan is also low, with the Pakistan Stock Exchange (PSX) having one of its worst-performing years in 2022, and the current year has not been great either. Recent events are likely to further dent the PSX's performance.

Meanwhile, the country is facing a challenging time in resuming the $6.5 billion bailout program from the IMF. The program has stalled due to the government's inability to meet certain loan conditions. Political tensions ahead of the upcoming elections add to the risk of a delay in the loan. The former premier’s arrest will only worsen the situation. The country is seeking to engage with the IMF beyond June, to secure additional financing from other multilateral and bilateral partners, which could reduce default risk. Pakistan's gross external financing needs are estimated to increase to 139.5% in fiscal year 2024, up from 133% in 2023.

Despite the historic low in civil-military relations, the immediate concern in Pakistan is the risk of default. Moody's ratings agency has already issued a warning, which should prompt those in power to take action. However, the chances of a deal seem low due to a lack of cohesion. Further, the arrest of Khan could exacerbate the situation, potentially leading to an economic meltdown in the country.