Pakistan’s banking sector has once again come into the spotlight, with the ongoing debate on its stability sparking a reaction among the public. Recently, the rumor mill went in overdrive, as a statement made by the State Bank of Pakistan’s (SBP) Deputy Governor, Dr. Inayat Hussain, regarding the depositor protection fund, was taken out of context. The fund essentially provides insurance coverage of up to 500,000 for commercial bank depositors.

However, the SBP promptly addressed the situation, emphasizing that the country's banking sector remains strong. They highlighted that 94% of depositors are fully protected under the Deposit Protection Act of 2016.

1/2 #SBP clarifies that bank deposits are perfectly safe owing to a sound banking system in Pakistan under a robust regulatory and supervisory framework. See PR: https://t.co/zLD1B94RdO#SBPClarification pic.twitter.com/d6O2hu9Dun

— SBP (@StateBank_Pak) October 5, 2023

Further, to build on its argument of stability of the banking system, the Central Bank states, “The sector posted a strong profitability of Rs 284 billion in first half of CY23, which is almost 125 percent higher than the first half of CY22. The higher earnings, in turn, also strengthened the capital of banks and the Capital Adequacy Ratio (CAR) of the banking sector increased to 17.8 percent by end June 2023 compared to 16.1 percent as of end June 2022, substantially higher than SBP’s minimum regulatory requirement of 11.5 percent and international standard of 10.5 percent. With improvement in solvency buffers, the ability of the banking sector to withstand a set of severe shocks has further improved.”

While the SBP pointed out in all the right directions to reinforce the stability of the banking sector, it overlooked a crucial threat to the sector’s liquidity, which is the exposure to government debt. Over the past 18 months, the discourse has repeatedly come back to the fact that a significant portion of the government's borrowing is from domestic banks. With rising interest rates and limited fiscal space, the possibility of a potential debt restructuring increases, leaving the banks vulnerable.

In Pakistan, a significant portion of banking resources are directed towards government lending as it provides a lucrative avenue to generate profits with minimal effort and an ever-present demand due to the government's substantial fiscal deficit.

Further, a segment of the banking sector, Microfinance Banks also need to be considered as a part of this debate given that it has a depositor base of more than 90 million. Therefore, we delve deeper into an analysis of these areas to determine whether the perceived stability has a strong foundation or if it is merely a cover-up.

The Sovereign-Bank nexus

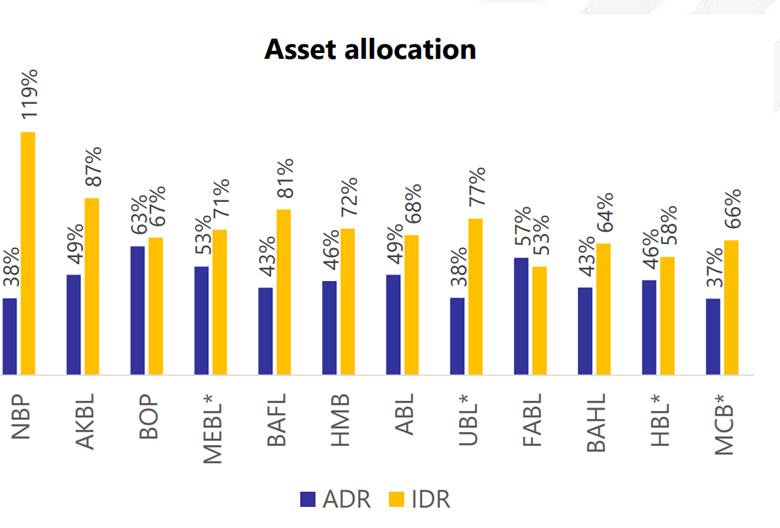

The primary risk to the banking sector, as previously mentioned, lies in its exposure to government securities. In Pakistan, a significant portion of banking resources are directed towards government lending as it provides a lucrative avenue to generate profits with minimal effort and an ever-present demand due to the government's substantial fiscal deficit. This imbalance is evident in the disparity between the conventional Advance to Deposit ratio (ADR) and the Investment to Deposit Ratio (IDR), with the latter being dominated by investments in government securities.

Source: JS Global

The problem arises from the fact that the government has accumulated significant amounts of debt from private banks. As a result, in the prevailing high interest environment, servicing this debt is increasingly consuming a significant portion of tax revenue and necessitating the imposition of harsh austerity measures, including cuts to public spending.

Now, before revisiting the SBP's official statement, it is crucial to understand a key term known as the Capital Adequacy Ratio (CAR). This ratio serves as a measure of a bank's ability to withstand losses through its capital. It also considers the associated risks of different asset classes, such as loans and investments.

The SBP understandably presents the CAR as a measure of stability. However, there is a noteworthy caveat: this figure does not account for the risks associated with investments in government securities, which happen to be the largest exposure for the private banking sector.

The problem arises from the fact that the government has accumulated significant amounts of debt from private banks. As a result, in the prevailing high interest environment, servicing this debt is increasingly consuming a significant portion of tax revenue and necessitating the imposition of harsh austerity measures, including cuts to public spending.

As per the World Bank’s Pakistan Development Update October 2023, “The aggregate commercial banks’ CAR stood at 16.3 percent in March 2023, dropping from 17 percent in December 2022. While this is still well above the minimum regulatory requirement (11.5 percent), several smaller banks remain undercapitalized. Additionally, the CAR does not adequately reflect the risks of banks’ exposure to the Government, which receives a zero-risk weight. The economic slowdown is further impacting the asset quality of banks. The ratio of non-performing loans (NPLs) to total lending has increased marginally to 7.8 percent in March 2023 from 7.5 percent in June 2022. While 90.7 percent of NPLs are provisioned for, risks are fast emerging, with many banks showing an accelerated rise in NPLs.”

This, however, raises the question of how resilient and strong the banking sector is and whether it can withstand a haircut if the government chooses to restructure its domestic debt.

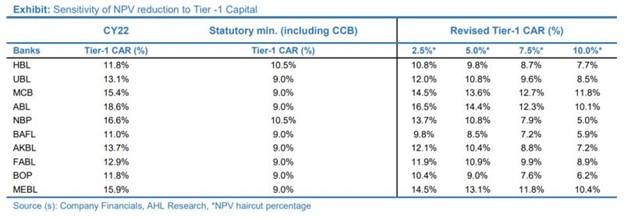

As per a report published by Arif Habib Limited in May 2023, “According to the analysis, every 5% NPV reduction (PKR 1.3 trillion) erodes Tier-1 CAR of coverage banks by 292bps. Based on the workings below, Tier 1 CAR of 5-7 out of 10 coverage banks falls below minimum threshold if NPV haircuts are more than 5%, while 2 out of 10 banks will face a capital call at even 5% NPV haircut.”

The Microfinance Banks

If the analysis above paints a bleak picture, the worst is yet to come. Despite having a small share of the total banking deposits, Pakistan's Microfinance Banks (MFBs) continue to be a significant player in the financial landscape. These banks cater to millions of customers, many of whom hail from low-income backgrounds.

This risk in the microfinance sector is so high that it was acknowledged by the International Monetary Fund (IMF), which in the Standby Agreement (SBA) signed in June this year barred the State Bank from extending the depositor protection scheme to the customers of these banks.

MFBs have faced ongoing challenges in developing a sustainable business model, with their difficulties exacerbated by the impact of the Covid-19 pandemic. Furthermore, the devastating floods that occurred last year had a significant effect on the agriculture sector, which happens to be the primary loan portfolio segment for these banks.

This risk in the microfinance sector is so high that it was acknowledged by the International Monetary Fund (IMF), which in the Standby Agreement (SBA) signed in June this year barred the State Bank from extending the depositor protection scheme to the customers of these banks.

“Staff noted the need to postpone the envisioned extension of the deposit insurance framework to microfinance banks until vulnerabilities within the sector have been addressed,” read the IMF’s report.

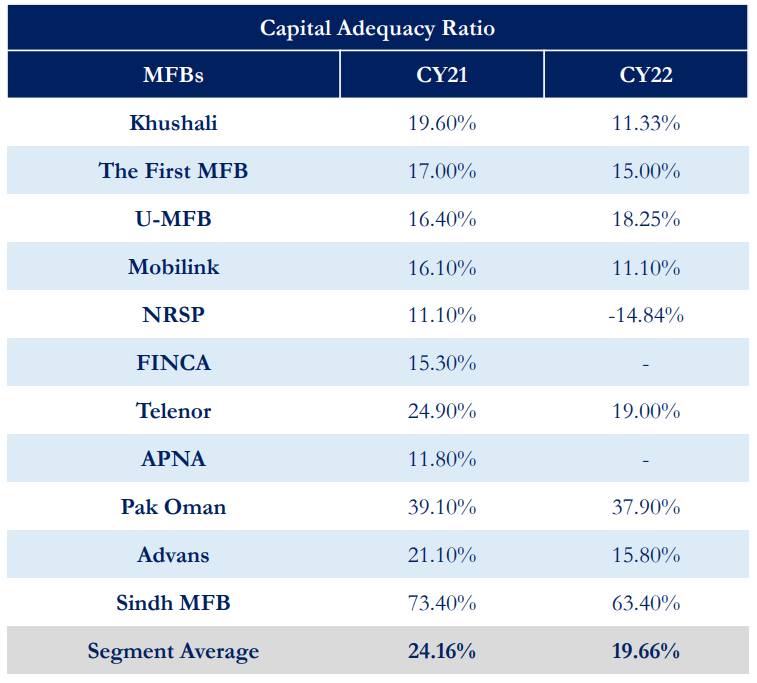

Further, as per a sector study conducted by Pakistan Credit Rating Agency (PACRA), “MFBs’ Average CAR was recorded at 19.66% in Calendar Year (CY)22 (24.16% in CY21). However, excluding the small-sized banks (Advans, Pak Oman, and Sindh MFB), the Sector’s average CAR dropped to ~9.97% (below statutory limit) during the same period.”

Source: PACRA

While significant vulnerabilities exist within the system, it is important to note that the (SBP) has historically demonstrated competence in effectively managing these challenges. It is noteworthy that in the financial history of the country, depositors have never experienced losses as a result of a bank's insolvency.

Additionally, when considering domestic debt restructuring, the probability of it occurring remains relatively low. This is because for the government, it would be seen as a measure of last resort. Prior to pursuing restructuring, the government would likely exhaust efforts to generate more revenue through the existing system, in order to create the much-needed fiscal space.