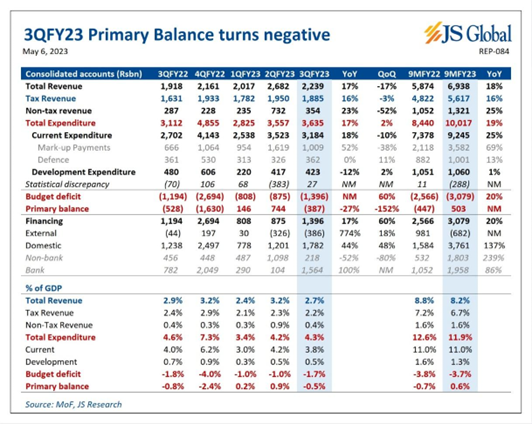

The Pakistani finance ministry has recently released the fiscal activity figures for the first nine months of the current fiscal year. Accordingly, the country's total revenue stood at Rs 6.9 trillion, with tax revenue contributing Rs 5.6 trillion and non-tax revenue contributing Rs 1.3 trillion. Total expenditure was Rs 10. trillion, resulting in a budget deficit of approximately Rs 3.1 trillion. The government financed the budget deficit with around Rs 3.8 trillion in domestic borrowing.

As reported by the Express Tribune, The Pakistani government has paid Rs 3.1 trillion in domestic debt servicing, which accounts for 87% of the total debt servicing. This emphasizes the need for restructuring both domestic and external debts to avoid the risk of default. However, finance minister Ishaq Dar has rejected the idea of debt restructuring.

While external debt restructuring has received significant attention and the G-20 has been undertaking to efforts develop a better framework for such restructurings, there is also a pressing need to address domestic debt restructuring issue. This conversation is equally important, given the precarious financial condition of the country and the massive domestic debt stock it has accumulated.

Domestic Restructuring

Domestic debt restructuring refers to the process of re-organizing or modifying the terms and conditions of a country's outstanding domestic debt obligations and is usually done in response to a country's inability to meet its debt obligations. The restructuring may involve changing the interest rate, maturity date, and principal amount of the debt, and may also include debt forgiveness or debt-for-equity swaps.

A recent report by Arif Habib Limited (ARHL), in response to the market chatter about restructuring domestic debt, analyzed the viability of any such effort.

To address whether Pakistan should undergo domestic debt restructuring, the ARHL report suggests answering three critical questions. These include evaluating whether the public debt-to-GDP ratio is unsustainable or fast approaching unsustainable levels, assessing how robust the financial system is to withstand any restructuring exercise, and identifying and mitigating the social and economic costs of restructuring.

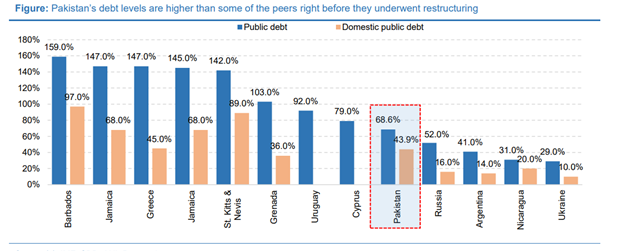

Source: ARHL (Public Debt as % of GDP)

The report highlights that Pakistan's domestic debt has more than doubled in the last five years, standing at Rs 33.8 trillion as of December 2022, while total public debt is Rs 52.5 trillion. While these statistics are concerning, the primary issue lies in the structure of the federal fiscal account. The federal government has been unable to expand its revenue base, improve tax administration and recovery, and reduce expenditures, including resolving loss-making state-owned enterprises (SOEs).

Pakistan's domestic debt structure comprises short-term and long-term debt instruments, with the government relying heavily on Pakistan Investment Bonds (PIBs) and Treasury Bills to finance its budget deficits and development projects. The report highlights a surge in mark-up payments, which have increased by 77% YoY in 1H FY23, further straining Pakistan's debt burden.

The report proposes various measures to reduce Pakistan's debt burden, such as revisiting the revenue-sharing ratio set forth by the NFC award of 2010, rationalizing federal expenses, and implementing a system to monitor and evaluate federal and provincial expenses to ensure effective and efficient use of resources.

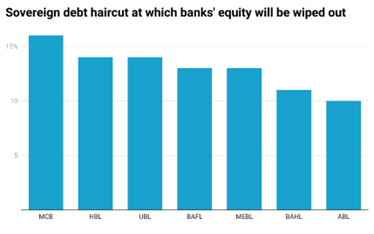

However, the fallout from domestic restructuring would primarily impact the local banking sector which holds more than 50% of the domestic debt. “The impact on bank’s balance sheet could be significant given treasuries constitute 46% of the total banking sector assets and 8.4x equity. Any loss in the value of the government treasuries shall lead to capital losses and brings into question the degree of capitalization of the sector and the amount of capital buffers available. A case in point is Greece (2012) where a 53% haircut for the banking sector resulted in a loss of 170% to the core Tier 1 capital,” the ARHL report said.

Source: JS Research

However, experts have also pointed out to alternatives that can serve to reduce the fiscal burden of debt servicing without disrupting the domestic banking system.

The case being presented is that around 40 percent of the domestic debt is owed to the State Bank of Pakistan (SBP) and the majority of the interest earnings on this debt will route back to the national treasury.

“The interest payments that are made by the finance ministry to the SBP make their way back to the government in the form of non-tax revenue when the State Bank makes a profit on those loans and then pays it back to the government in the form of a dividend. This basically means, the government is paying itself for a loan it gives itself – money from one hand into the other and back into the first,” writes Journalist Ariba Shahid in an article for Profit.

However, the other group of lenders, commercial banks, leverage depositors’ money to lend to the government.

“Approximately Rs14 trillion of bank deposits are interest bearing where banks are bound to pay 15.5 percent (150 bps below the policy rate) with exception of Islamic deposits where the return is slightly lower. Here, banks are raising deposits at minimum 15.5 percent and lending it to the government at 17-18 percent. If interest rates move up further, banks’ margins will remain the same while depositors will benefit incrementally,” wrote finance and economy journalist Ali Khizar back in February 2023.

Source: JS Research

In the same article, Ali has suggested that the government can raise taxes on these depositors and bridge the fiscal gap through incremental revenues. The downside to this would be in the shape of disincentivizing savings and encouraging the informal economy which can further aggravate the country’s economic woes.

However, if the government chooses to proceed with domestic debt restructuring then the process, as per former World Bank Economist Dr. Arshad Zaman, would involve six steps. These include: (i) disaggregating debt stock, (ii) identifying exactly the domestic debt to be restructured and estimating the gross debt relief target (DRT) necessary to restore debt sustainability, (iii) deducting the associated fiscal costs (recapitalization of financial institutions, subsidies, etc.) to achieve the net DRT, (iv) assessing the wider economic costs associated with restructuring, (v) ensuring that the State Bank of Pakistan, including the payments system, can operate normally throughout and (vi) determining which claims to restructure to minimize overall costs.

Nevertheless, any decision on debt restructuring will require careful consideration of its impact on the economy and the banking sector. It remains to be seen how the Pakistani government will proceed in this regard.