Pakistan is currently facing several economic challenges that require immediate action, including acute shortages of foreign currency, a drastic depreciation of the Pakistan rupee's value, and an increase in energy prices. In light of these challenges, the government has been forced to seek external help to keep the economy afloat.

Unfortunately, the recent internet connectivity blackout across Pakistan's major cities has further worsened the economic situation. After the arrest of Imran Khan, chairman of PTI, several cities witnessed widespread violence and protests.

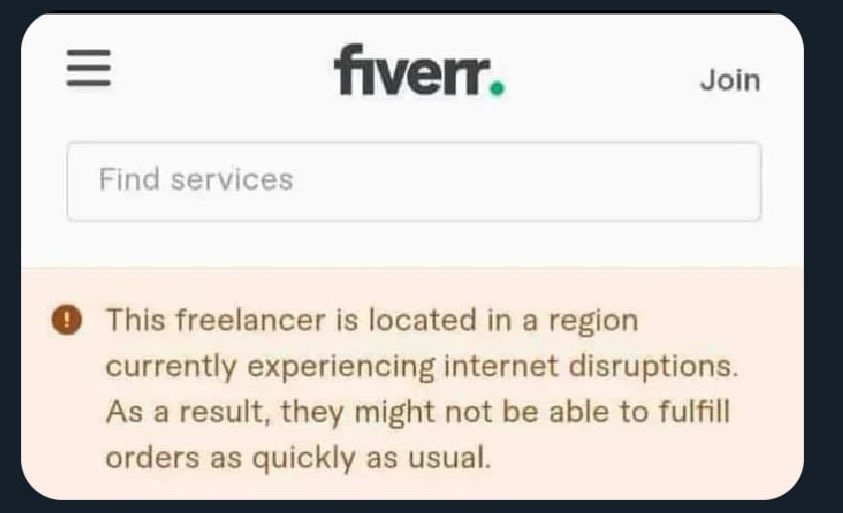

The suspension of mobile broadband services by the Pakistan Telecommunication Authority at the direction of the Interior Ministry exacerbated the economic issues, resulting in commercial activity coming to a standstill, and many businesses remained closed on May 9 and 10. The suspension of internet services has affected the IT freelance industry, which lost almost $2 million a day.

In addition, as reported by Reuters, point-of-sale transactions routed through the country's major digital payment systems declined by 50%. The primary reasons for the reported slump were the suspension of mobile internet services and lower footfall at stores due to the political turmoil. As a result, international payment card transactions through 1LINK on May 10 were down 45% in volume, and 46% in value.

Transactions on Pakistan's domestic payment scheme, PayPak, were also down 52% in volume and 56% in value. All these developments have created a negative image for Pakistan's IT sector, which can affect the country's IT business prospects in the future.

The ongoing economic challenges, along with the political instability, have also pushed foreign investors away from the country. Pakistan's profit outflow during July-March this year decreased by 81.6% to $233 million compared to $1.27 billion in the same period last year, which has been attributed to the uncertain political and economic situation in the country.

The country is also facing difficulty in resuming the $6.5 billion bailout program from the International Monetary Fund (IMF), which has stalled due to the government's inability to exhibit the required fiscal discipline.

The risk of a delay in the loan has increased due to the political tensions ahead of the upcoming elections. Hence, Pakistan aims to engage with the IMF beyond June to secure additional financing from other multilateral and bilateral partners to reduce default risk. Moody's has expressed concern about the situation, stating that the country will require external help to stay afloat in the next few years, as reconstruction efforts from last year's floods and monumental debt service payments have burdened the economy.

No freelance income for you!

Consequently, $2.7 billion worth of assistance is stuck in the pipeline as the Fund staff seeks guarantees of fiscal discipline in the next fiscal budget. The IMF's concern is understandable given the country's track record of stop-go policies and the upcoming general election, which will create incentives for irresponsible fiscal spending.

Despite talks of possible sovereign default, the current Finance Minister appears unfazed. Dar has stated that Pakistan will remain financially stable, with or without the assistance of the IMF. The Minister's statement comes after news of the IMF asking the government to scrap the proposed fuel cross-subsidy scheme.

Therefore, to achieve macroeconomic stability, Pakistan must avoid economic decision-making based on political expediency. The government must take decisive steps to stabilize the economy, curb the budget deficit and implement necessary tax reforms.

The challenges Pakistan faces must be addressed with the support of all stakeholders, including the government, investors, and international financial institutions.

Greater government accountability and fiscal discipline are necessary to secure a stable economic future, given the country's reliance on external funding. All concerned parties must take urgent action to revive the country's economy and restore investor confidence.