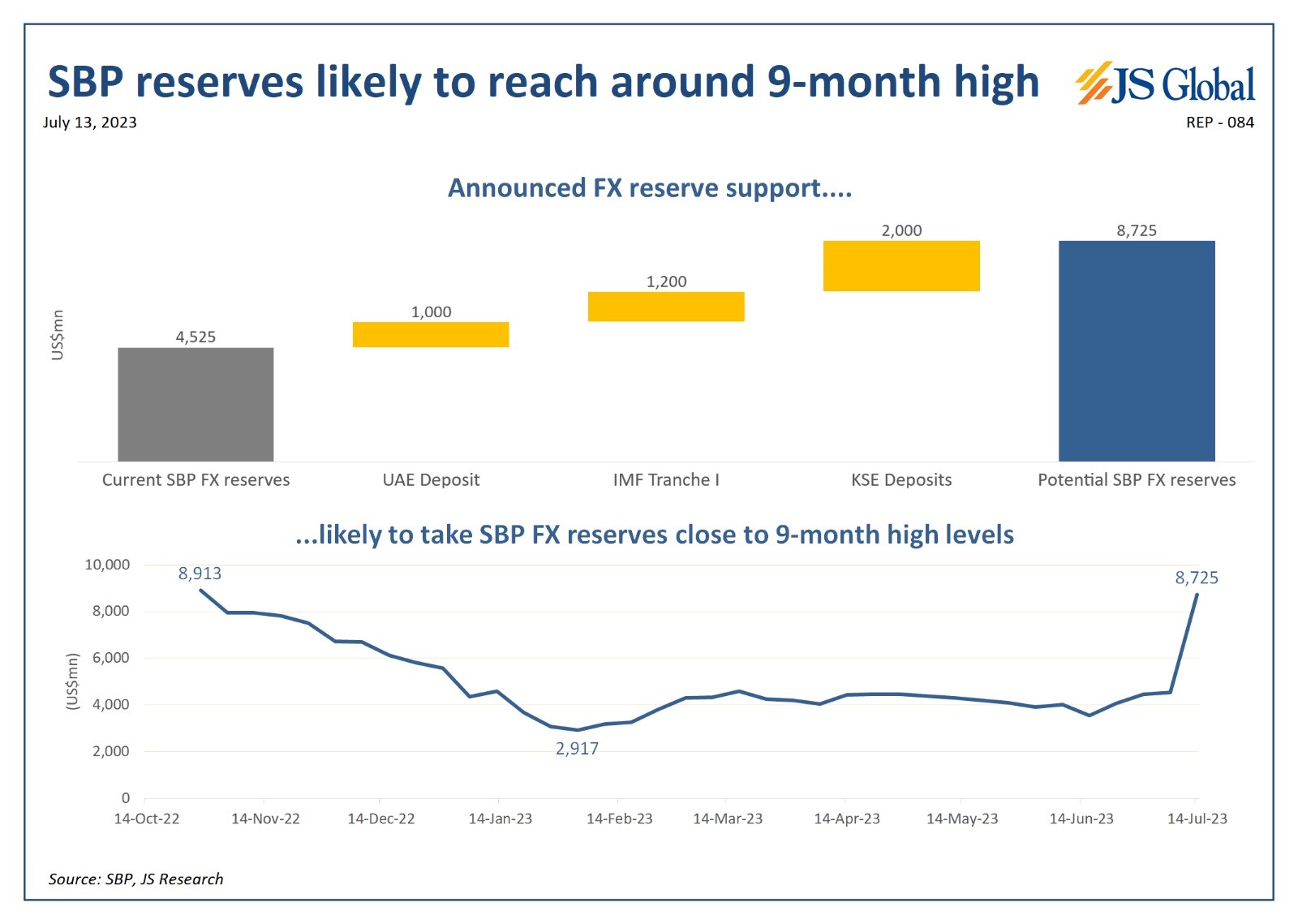

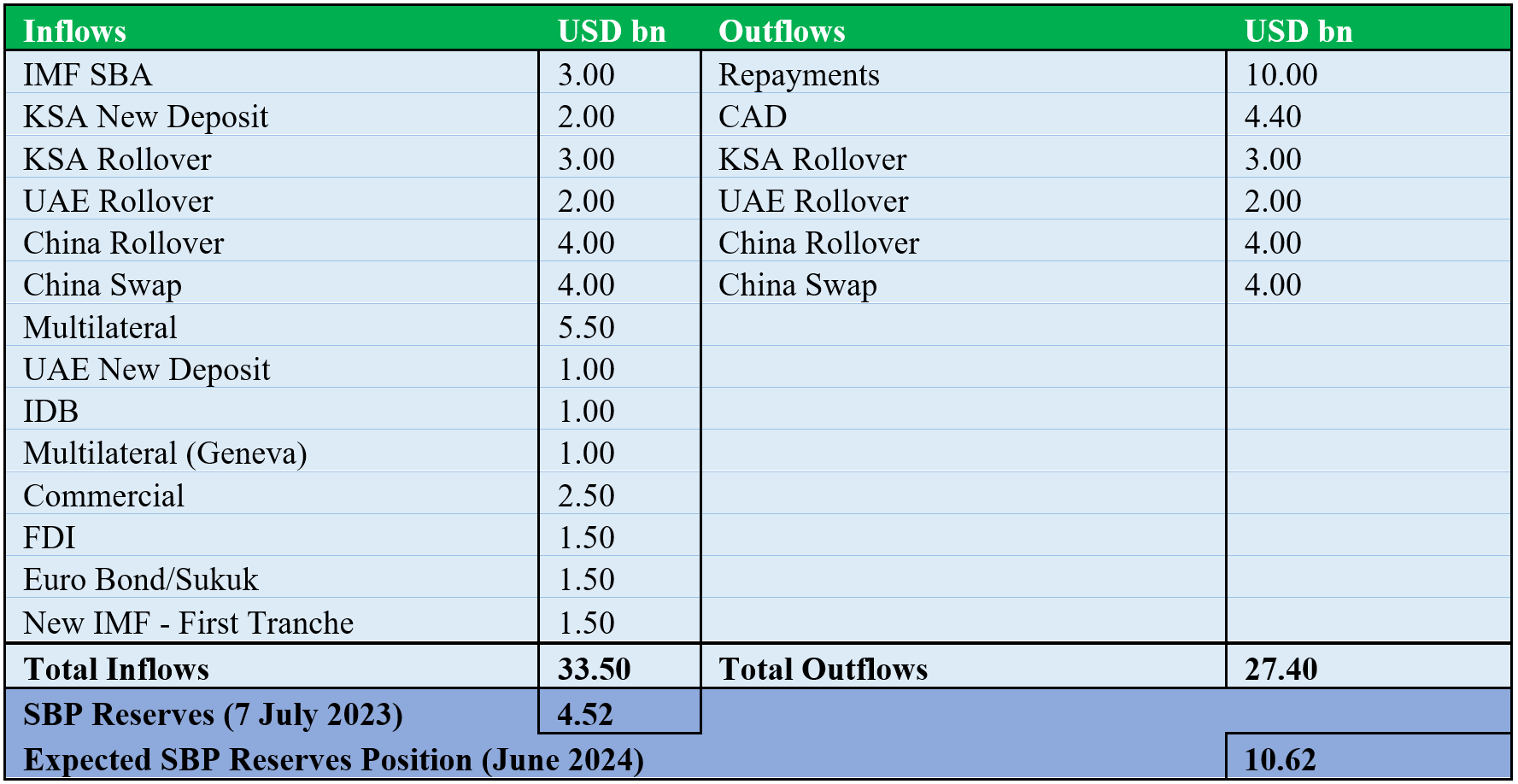

The first half of July witnessed Pakistan's remarkable economic progress across various fronts. The country's initial breakthrough with the IMF, followed by the successful funding of the promised tranche and bilateral support, has led to a surge in forex reserves and alleviated concerns about default at least for this calendar year. Additionally, the reassurance from the Prime Minister regarding timely elections, combined with the infusion of funding, has rejuvenated the country's stock market, which is displaying positive trends. Moreover, the Pakistani rupee has responded positively to these economic developments and has gained some ground against the greenback.

However, as we move into the second half of the year, it becomes crucial to comprehend the country's economic reality and the underlying fundamentals.

The Outlook

According to a recently published report titled "Resurgence of Optimism" by Arif Habib Limited (ARHL), the upcoming elections in October or November 2023 are expected to bring an end to the prolonged period of political uncertainty. The completion of the constitutional term of the National and Provincial Assemblies, with Punjab and KPK already dissolved earlier in August 2023, will be followed by elections within three months.

The successful conduct of these elections is anticipated to mark the end of over a year of political instability. The report suggests that a newly elected government will likely be in a better position to make improved economic policy decisions, including the successful negotiation of a new IMF program.

Therefore, the financial markets are expected to react positively to the new political setup, as elections will bring clarity to the political arena and enable more decisive economic decisions that address structural issues. It is also anticipated that negotiations for a new IMF program will commence once the ongoing Stand-By Arrangement ends, while interest rate cuts are expected in February or March 2024. According to the report, the key factors that could sustain a rally in the stock market include political stability and monetary easing.

At the macro level, Pakistan is likely to face further challenges due to historical tendencies. According to the analysis conducted by ARHL, the country experienced a significant decline in international trade during Fiscal Year (FY) 2023, with a staggering 43% year-on-year decrease in the trade deficit.

This decline can be attributed to a mix of factors, including tight macroeconomic policies, administrative measures, and the global recession. Despite the impact of floods on the Current Account Deficit (CAD), the overall effect has been relatively muted so far. Slower domestic growth, lower global commodity prices, and the offsetting impact of higher food and cotton imports, along with lower textile exports, have helped mitigate the impact.

However, the report notes that there are downside risks on the export front moving forward, primarily due to the global recession that could negatively impact exports. While a gradual easing of import restrictions is expected in FY24, in line with the IMF's discouragement of such measures, the tight macroeconomic policies in place indicate that the current account deficit is likely to remain around $4.4 billion, which is equivalent to 1.2% of GDP. Although concerns persist regarding commodity markets, particularly food and fuels, international prices are expected to remain low due to growing global recessionary fears. Therefore, no significant increase is forecasted in these categories moving forward.

Source: ARHL

Investor Optimism

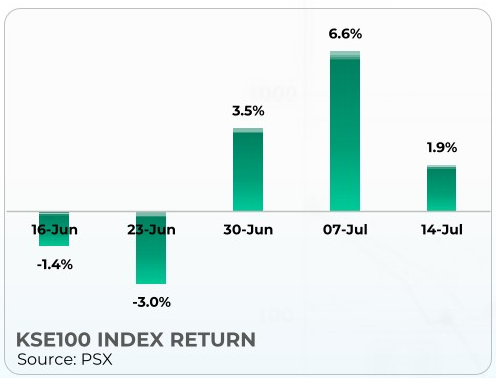

The KSE-100 Index, Pakistan's benchmark share index, currently has one of the lowest price-to-earnings ratio in the world at around 4 times. This significant drop in valuations, as per Bloomberg, could potentially attract buyers who had previously abandoned the market due to turmoil.

Further, the Bloomberg report states that market watchers had already factored in the low probability of Pakistan receiving loan from the IMF, so the recent positive surprise in this regard could lead to a sustain growth in stock values.

Graph Source: KTrade

However, as per a report by KTrade, inflation is expected to remain high in the upcoming fiscal year (FY24) due to structural adjustments, including increases in energy tariff rates, with a possible Rs. 5-7/kWh hike in the base power tariff and a 50% rise in gas tariffs. The IMF estimates that the Consumer Price Index (CPI) will hover around 26% in FY24. These figures may lead the SBP to further raise interest rates in order to maintain positive real interest rates. This would lead to a dampening impact on the market.

https://twitter.com/FRIMVentures/status/1679760276294610944

Therefore, foreign investors continue to be cautious about investing in the country due to elevated country risk resulting from a variety of factors. These include political instability, economic risks such as recessionary conditions and high inflation, concerns about sovereign debt burdens and the probability of default, ongoing currency fluctuations, and adverse government regulations such as expropriation or currency controls.

However, as we move into the second half of the year, it becomes crucial to comprehend the country's economic reality and the underlying fundamentals.

The Outlook

According to a recently published report titled "Resurgence of Optimism" by Arif Habib Limited (ARHL), the upcoming elections in October or November 2023 are expected to bring an end to the prolonged period of political uncertainty. The completion of the constitutional term of the National and Provincial Assemblies, with Punjab and KPK already dissolved earlier in August 2023, will be followed by elections within three months.

The successful conduct of these elections is anticipated to mark the end of over a year of political instability. The report suggests that a newly elected government will likely be in a better position to make improved economic policy decisions, including the successful negotiation of a new IMF program.

Therefore, the financial markets are expected to react positively to the new political setup, as elections will bring clarity to the political arena and enable more decisive economic decisions that address structural issues. It is also anticipated that negotiations for a new IMF program will commence once the ongoing Stand-By Arrangement ends, while interest rate cuts are expected in February or March 2024. According to the report, the key factors that could sustain a rally in the stock market include political stability and monetary easing.

At the macro level, Pakistan is likely to face further challenges due to historical tendencies. According to the analysis conducted by ARHL, the country experienced a significant decline in international trade during Fiscal Year (FY) 2023, with a staggering 43% year-on-year decrease in the trade deficit.

This decline can be attributed to a mix of factors, including tight macroeconomic policies, administrative measures, and the global recession. Despite the impact of floods on the Current Account Deficit (CAD), the overall effect has been relatively muted so far. Slower domestic growth, lower global commodity prices, and the offsetting impact of higher food and cotton imports, along with lower textile exports, have helped mitigate the impact.

However, the report notes that there are downside risks on the export front moving forward, primarily due to the global recession that could negatively impact exports. While a gradual easing of import restrictions is expected in FY24, in line with the IMF's discouragement of such measures, the tight macroeconomic policies in place indicate that the current account deficit is likely to remain around $4.4 billion, which is equivalent to 1.2% of GDP. Although concerns persist regarding commodity markets, particularly food and fuels, international prices are expected to remain low due to growing global recessionary fears. Therefore, no significant increase is forecasted in these categories moving forward.

Source: ARHL

Investor Optimism

The KSE-100 Index, Pakistan's benchmark share index, currently has one of the lowest price-to-earnings ratio in the world at around 4 times. This significant drop in valuations, as per Bloomberg, could potentially attract buyers who had previously abandoned the market due to turmoil.

Further, the Bloomberg report states that market watchers had already factored in the low probability of Pakistan receiving loan from the IMF, so the recent positive surprise in this regard could lead to a sustain growth in stock values.

Graph Source: KTrade

However, as per a report by KTrade, inflation is expected to remain high in the upcoming fiscal year (FY24) due to structural adjustments, including increases in energy tariff rates, with a possible Rs. 5-7/kWh hike in the base power tariff and a 50% rise in gas tariffs. The IMF estimates that the Consumer Price Index (CPI) will hover around 26% in FY24. These figures may lead the SBP to further raise interest rates in order to maintain positive real interest rates. This would lead to a dampening impact on the market.

https://twitter.com/FRIMVentures/status/1679760276294610944

Therefore, foreign investors continue to be cautious about investing in the country due to elevated country risk resulting from a variety of factors. These include political instability, economic risks such as recessionary conditions and high inflation, concerns about sovereign debt burdens and the probability of default, ongoing currency fluctuations, and adverse government regulations such as expropriation or currency controls.