While the International Monetary Fund’s (IMF) recent report has pointed out the fault lines in Pakistan’s economic fundamentals, it has also specifically mentioned the vulnerabilities of the country’s microfinance sector.

“Staff noted the need to postpone the envisioned extension of the deposit insurance framework to microfinance banks until vulnerabilities within the sector have been addressed,” read the report.

By postponing the extension of the deposit insurance framework to microfinance banks, the customer base of the microfinance sector, which largely consists of financially marginalized communities in Pakistan, would be exposed to the additional risks associated with the sector's vulnerabilities.

While this news may be disappointing for the sector, there have been recent positive developments. Kashf Foundation, for instance, launched a gender bond earlier this month to raise funds and enhance liquidity, with the goal of expanding loan disbursements to support the advancement, empowerment, and equality of women.

However, before delving into the impact of these developments, it's important to understand the current standing of the microfinance sector and the various business models it relies on.

Pakistan’s microfinance sector

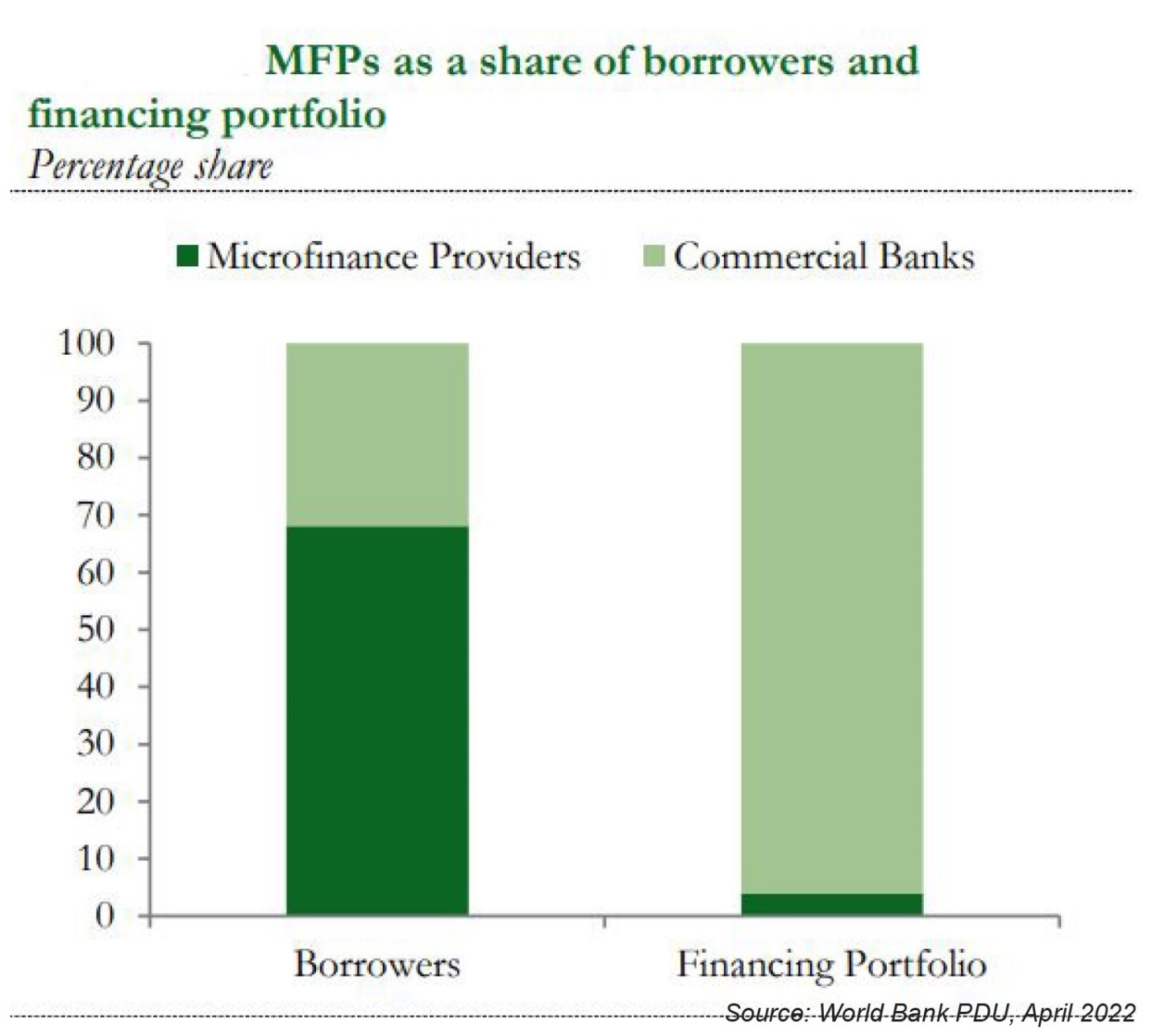

According to the World Bank, “The microfinance sector, a driver of Pakistan’s financial inclusion agenda, serves 76% of all borrowers from the financial sector and accounts for approximately a third of all outstanding agriculture advances. The sector has been deeply affected by the combined impact of the COVID-19-related economic slowdown and mitigation measures, and the devastating floods of 2022.”

As per a report by Pakistan Credit Rating Agency (PACRA), the Microfinance Sector in Pakistan is classified into three segments: Microfinance Banks (MFBs), Microfinance Institutions (MFIs), and Rural Support Programs (RSPs). The sector consists of 11 MFBs, 17 MFIs, 4 RSPs, and 4 other institutions. MFBs have the largest market share in terms of loan portfolios. The main investors in the country's microfinance sector include commercial banks, telecommunication companies, nonprofit entities, and specialized microfinance institutes.

On the performance front, according to a report by the Pakistan Microfinance Network, the microfinance industry has achieved a gross loan portfolio of over Rs. 500 billion. The number of active borrowers has increased to 9.3 million, with Microfinance Banks (MFBs) serving 6.1 million borrowers and Non-Banking Microfinance companies serving 3.2 million.

According to the World Bank, “The microfinance sector, a driver of Pakistan’s financial inclusion agenda, serves 76% of all borrowers from the financial sector and accounts for approximately a third of all outstanding agriculture advances. The sector has been deeply affected by the combined impact of the COVID-19-related economic slowdown and mitigation measures, and the devastating floods of 2022.”

On the deposits front, the number of depositors has reached 98 million. Mobilink Microfinance Bank and Telenor Microfinance Bank continue to dominate the market, primarily due to the popularity of their respective mobile wallet applications, Jazz Cash and EasyPaisa. These two banks have a combined active saver base of 81 million.

While in terms of value, Khushhali Bank, by the end of 2022 has a deposit portfolio of Rs. 96 billion, representing 17% of the market, only behind HBL Microfinance Bank which has a 23% deposit market share at a value of Rs. 110 billion.

Vulnerabilities

According to the World Bank Pakistan Development Update for April 2023, the percentage of the portfolio at risk in microfinance banks increased from 4.5% to 5.9% of the total portfolio. This refers to loan installments which were overdue for more than 30 days. Additionally, around 18% of borrowers and 40% of loans in the microfinance sector were in flood-impacted areas, adding strain to the sector's loan book quality.

Microfinance banks at the sectoral level are currently facing undercapitalization, with a decline in their capital adequacy ratio (CAR) from 14.9% in June 2022 to 11.7% in September 2022. This indicates a severe liquidity crunch which threatens the fundamental business model of the commercial players in the sector.

Though the capital adequacy situation has improved slightly, compared to the last year, it is by no means adequate enough to mitigate the risk to an acceptable level, as exogenous shocks like the Covid pandemic and more recently, the floods have shown how fragile the sector’s foundations are.

If this risk materializes and leads to the closure of an MFB, depositors could potentially lose their money without any recourse as the IMF directive has stripped them of regulatory protection.

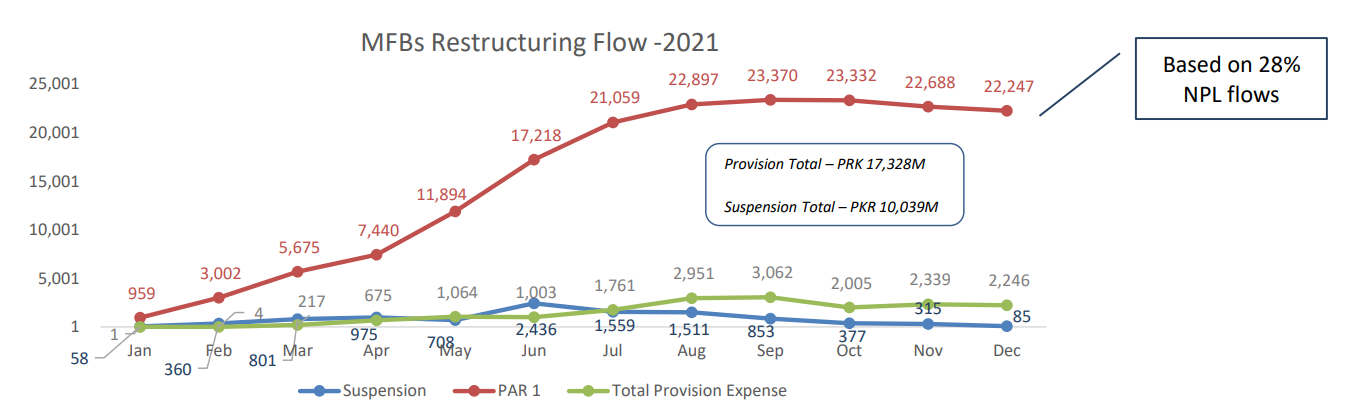

MFB’s assessment in 2021 of recoverability of Covid era restructured loans

Sector’s response

While the risk of loan default has surged in the past few years, it is necessary to mention that the sector has for most part of its existence has struggled to put up a robust and profitable business model.

Therefore, acknowledging the limitations at this front, different players have significantly diverted their strategies from the core microfinance business.

The two-leading telco-backed microfinance operators, Telenor Bank and Mobilink Bank, have increased their focus on nano-lending, which offers small ticket loans for emergency or bridge financing. This option provides a safer alternative for consumers compared to the notorious digital loan sharks prevalent in the market.

Microfinance banks at the sectoral level are currently facing undercapitalization... This indicates a severe liquidity crunch which threatens the fundamental business model of the commercial players in the sector.

However, this concentration on nano-lending has resulted in a lack of financing options for Pakistan's rural population, which heavily relies on core microfinance lenders for much-needed financial assistance.

“What is somewhat ironic is how the industry for decades has presented itself as the harbinger of financial inclusion by giving credit and encouraging entrepreneurship. Yet the kind of amounts they are currently offering might not even be enough to cover a small business’s electricity bill,” writes Mutaher Khan in his article The nano-isation of microfinance loans, for Dawn.

On the contrary, the likes of U Microfinance Bank have opted for a more commercial banking approach of investing most of its resources in government securities rather than lending to the microfinance target audience.

The silver lining

While the banks struggle with non-performing loans (NPLs), Non-Banking Microfinance institutions (MFI) like Kashf Foundation have historically performed better on that front.

The reason being that MFIs are non-deposit taking entities and instead depend on raising debt to expand their loan portfolios. Thus, are more diligent as a high NPL ratio can hinder their ability to repay lenders and raise additional finance.

In this context, Kashf Foundation's Gender Bond of Rs. 2.5 billion emerges as a beacon of hope for the sector, which is currently facing a liquidity crunch. The bond is a privately placed capital market instrument that will subsequently be listed.

The new instrument stands out for its noteworthy feature of having Infrazamin Pakistan (IZP) providing a guarantee cover of Rs. 2.85 billion for investors, including 100% principal and one interest installment. According to the company's representatives, the purpose behind this borrowing initiative is to expand Kashf's investor base and establish Pakistan's first-ever 'Gender Bond.'

Further, IZP’s guarantee provides investors with protection against the risk of default by the underlying obligor, Kashf Foundation. Unlike conventional Term Finance Certificates (TFCs), where investors bear the entire default risk, IZP assumes this responsibility.

This structure helps address a common challenge in the microfinance sector, which is the difficulty in raising liquidity from the capital market. In Pakistan, most institutions in the sector have ratings within the A- to A+ range, which is considered non-investable. Typically, obligors would need to pledge cash or near-cash collateral to improve the rating of the instrument, which can further strain liquidity and is not aligned with the objective of raising funds from the capital market.

Yet its applicability for the sector as a whole and specifically for the MFBs remains a question. As per Mustafa Pasha, Chief Investment Officer, Lakson Investments, “Microfinance banks have faced challenges with loan losses, resulting in the need for significant equity injections in several cases. Therefore, caution should be exercised when considering investments in this sector. In addition to credit risk, it's important to note that instruments issued by the sector may also lack liquidity, similar to most corporate debt. As a result, potential investors must be prepared for the possibility of not being able to sell their investments at a favorable price if necessary.”