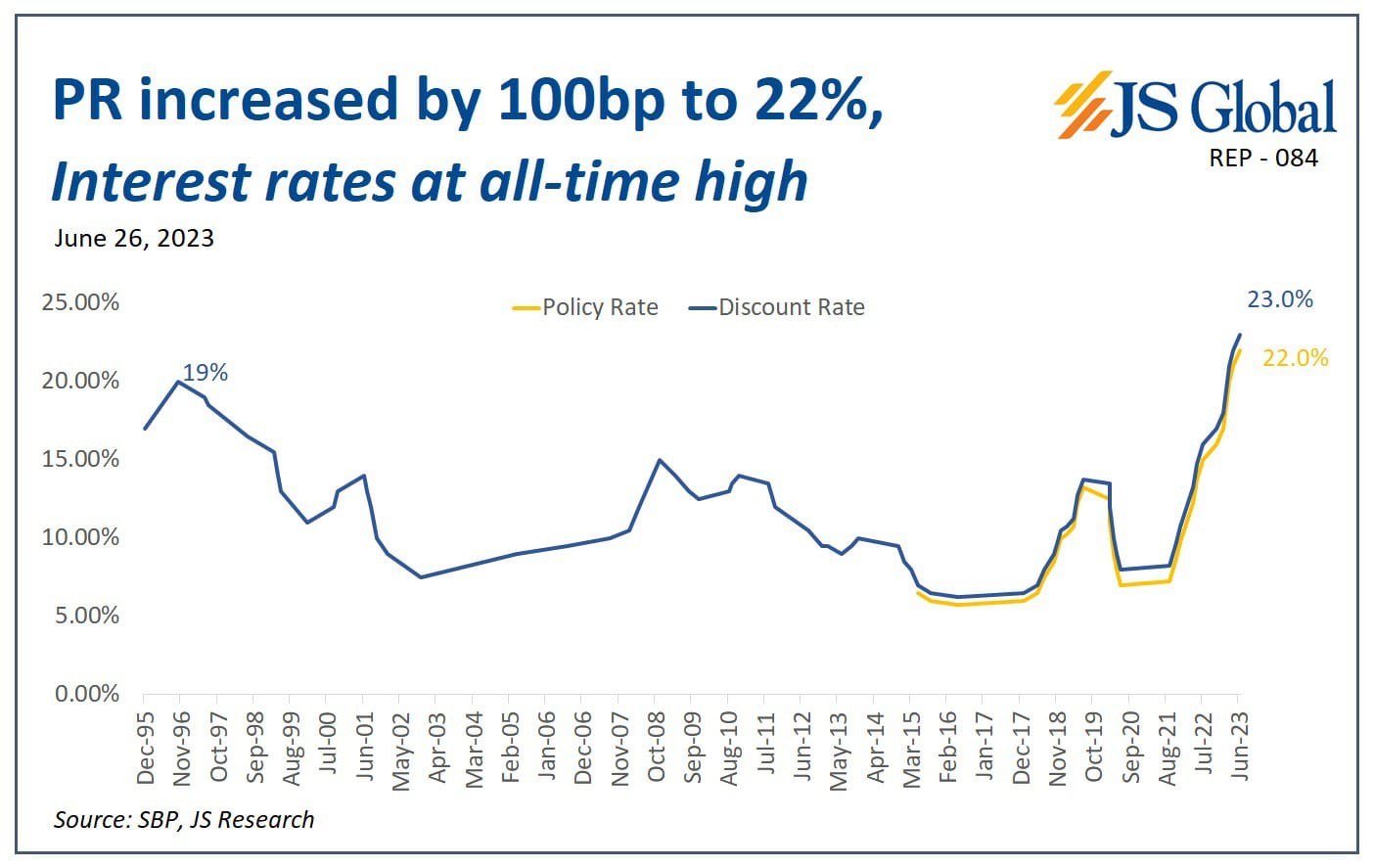

The State Bank of Pakistan (SBP) convened an emergency Monetary Policy Committee (MPC) meeting on Monday, June 26, 2023, in order to raise the interest rate by a further 1%.

In a press release, the Committee provided a rationale for the move, stating, 'The Committee believes that additional tax measures are likely to contribute to inflation both directly and indirectly. Meanwhile, a reduction in imports may exert pressure on the foreign exchange market, which could result in a higher-than-anticipated exchange rate pass-through to domestic prices.'

Despite the justification provided by the SBP, experts believe that the sudden interest rate hike is an attempt to meet the International Monetary Fund's (IMF) requirements, particularly after the SBP chose not to increase the policy earlier this month. This latest action adds to the list of measures taken by the government to revive the stalled $6.7 billion IMF program.

Further, the Pakistani stock market has experienced an exceptional rally following the release of revised budget figures that have increased the likelihood of the IMF program's revival. However, the sudden interest rate hike may have a dampening effect on stocks.

The Hard Choice

As per an article published by the IMF, “a guidepost for central bankers in setting the policy rate is the concept of the neutral rate of interest: the long-term interest rate that is consistent with stable inflation. The neutral interest rate neither stimulates nor restrains economic growth. When interest rates are lower than the neutral rate, monetary policy is expansionary, and when they are higher, it is contractionary.”

The need for a contractionary monetary policy in Pakistan stems from the fact that the country is facing high inflation that has been propelled by the floods last year. Further, the government is aiming to curb the fiscal deficit by curtailing demand.

“Proactive monetary policy to guide inflation to more moderate levels. Headline inflation exceeded 20 percent in June, hurting particularly the most vulnerable. In this regard, the recent monetary policy increase was necessary and appropriate, and monetary policy will need to be geared towards ensuring that inflation is brought steadily down to the medium-term objective of 5–7 percent,” read the IMF press release on reaching a staff-level agreement with Pakistan back in July 2022.

https://twitter.com/ThePBC_Official/status/1673307248918171650?t=O6knlRzrI2ekhlCxkD8MiQ&s=09

Back to the IMF

According to Bloomberg, Pakistan's recent measures have turned the tides in its favor, potentially allowing the country to avoid a sovereign default for the time being. The IMF’s $6.7 billion bailout package is set to expire on Friday, with $2.7 billion of loans pending approval.

The disbursement of these funds would provide a much-needed reprieve for Pakistan, which has been struggling with several crises and facing economic collapse this year. The country is battling record inflation, making it increasingly difficult for citizens to afford basic necessities such as fuel and food.

Additionally, foreign reserves are limited, and debt payments are looming. The IMF loans are critical because Pakistan is facing approximately $23 billion in external debt payments for the upcoming fiscal year, which is more than six times the country's foreign-exchange reserves. There is a $1.6 billion debt payment, including a $1 billion Chinese deposit, due in July, which is typically rolled over.

What about geopolitics?

The incumbent Finance Minister has been calling foul and blaming geopolitics as the reason for a stalemate with the Fund. His claims are true to an extent, as the IMF – the Western dominated lender of last resort has a clear leaning towards US allies, and Pakistan, one of the IMF’s most loyal creditors, has long been a beneficiary.

However, the recent chain of events prove that most of Dar’s claims have been exaggerations, which is evident from the fact that things have started moving again after the IMF’s diktats have been taken more seriously.

In a press release, the Committee provided a rationale for the move, stating, 'The Committee believes that additional tax measures are likely to contribute to inflation both directly and indirectly. Meanwhile, a reduction in imports may exert pressure on the foreign exchange market, which could result in a higher-than-anticipated exchange rate pass-through to domestic prices.'

Despite the justification provided by the SBP, experts believe that the sudden interest rate hike is an attempt to meet the International Monetary Fund's (IMF) requirements, particularly after the SBP chose not to increase the policy earlier this month. This latest action adds to the list of measures taken by the government to revive the stalled $6.7 billion IMF program.

Further, the Pakistani stock market has experienced an exceptional rally following the release of revised budget figures that have increased the likelihood of the IMF program's revival. However, the sudden interest rate hike may have a dampening effect on stocks.

The Hard Choice

As per an article published by the IMF, “a guidepost for central bankers in setting the policy rate is the concept of the neutral rate of interest: the long-term interest rate that is consistent with stable inflation. The neutral interest rate neither stimulates nor restrains economic growth. When interest rates are lower than the neutral rate, monetary policy is expansionary, and when they are higher, it is contractionary.”

The need for a contractionary monetary policy in Pakistan stems from the fact that the country is facing high inflation that has been propelled by the floods last year. Further, the government is aiming to curb the fiscal deficit by curtailing demand.

“Proactive monetary policy to guide inflation to more moderate levels. Headline inflation exceeded 20 percent in June, hurting particularly the most vulnerable. In this regard, the recent monetary policy increase was necessary and appropriate, and monetary policy will need to be geared towards ensuring that inflation is brought steadily down to the medium-term objective of 5–7 percent,” read the IMF press release on reaching a staff-level agreement with Pakistan back in July 2022.

https://twitter.com/ThePBC_Official/status/1673307248918171650?t=O6knlRzrI2ekhlCxkD8MiQ&s=09

Back to the IMF

According to Bloomberg, Pakistan's recent measures have turned the tides in its favor, potentially allowing the country to avoid a sovereign default for the time being. The IMF’s $6.7 billion bailout package is set to expire on Friday, with $2.7 billion of loans pending approval.

The disbursement of these funds would provide a much-needed reprieve for Pakistan, which has been struggling with several crises and facing economic collapse this year. The country is battling record inflation, making it increasingly difficult for citizens to afford basic necessities such as fuel and food.

Additionally, foreign reserves are limited, and debt payments are looming. The IMF loans are critical because Pakistan is facing approximately $23 billion in external debt payments for the upcoming fiscal year, which is more than six times the country's foreign-exchange reserves. There is a $1.6 billion debt payment, including a $1 billion Chinese deposit, due in July, which is typically rolled over.

What about geopolitics?

The incumbent Finance Minister has been calling foul and blaming geopolitics as the reason for a stalemate with the Fund. His claims are true to an extent, as the IMF – the Western dominated lender of last resort has a clear leaning towards US allies, and Pakistan, one of the IMF’s most loyal creditors, has long been a beneficiary.

However, the recent chain of events prove that most of Dar’s claims have been exaggerations, which is evident from the fact that things have started moving again after the IMF’s diktats have been taken more seriously.