The fortunes of the Pakistani rupee have changed spectacularly over the past three weeks. After breaching the 330 mark against the greenback in the open market and widening the gap to about 9% compared to the interbank market, there has been a significant reversal. Currently, both rates are hovering around 290, and experts are anticipating further appreciation in the coming weeks.

The string of appreciation began as the state initiated a crackdown on money exchange companies involved in hoarding and smuggling of the dollar. As a result, market sentiment regarding the currency has shifted, with exporters choosing official channels to clear their invoices and a significant channel correction occurring in foreign remittances.

However, there are concerns about the sustainability of the tight administrative controls without a change in the underlying fundamentals. Therefore, analyzing the current currency market situation requires considering the factors that led to the correction and what is necessary to maintain it.

Course correction

The open market, facilitated by money exchange companies, serves as a retail outlet for foreign exchange trading. It is primarily fueled by remittances and driven by individuals planning to travel abroad.

However, illicit activities have become commonplace in this market. Several participants engage in selling dollars to walk-in customers at a premium, keeping these transactions off the books and not reporting them to the SBP. This behavior is speculative and aims to generate quick profits for both parties. Consequently, it pushes the open market rate upwards. Additionally, exchange companies are a key player in the leakage of dollars to Afghanistan, which further depletes the dollar supply in the market and puts pressure on the exchange rate.

Given the increasing prevalence of these activities, the regulator had to take action to maintain parity between the interbank and open market rates in line with the agreement with the International Monetary Fund (IMF). Consequently, the Federal Investigation Agency (FIA) conducted a crackdown, arresting individuals involved in illegal trading.

FIA personnel were deployed outside major exchanges to monitor transactions, leaving market players with no option but to cease unrecorded transactions. As a result, individuals began redirecting their forex receipts to the interbank market, thereby increasing liquidity. Moreover, several money exchanges surrendered surplus dollars, likely originating from unrecorded transactions to the banks, further enhancing liquidity in the interbank market.

This was followed by exporters bringing in their forex receipts through the interbank market resulting in a flurry of dollars. Further, as the hawala/hundi market slowed down, remittances through the interbank market saw an uptick.

This has enabled a sustained run of appreciation with the open market rate now trailing behind the interbank rate.

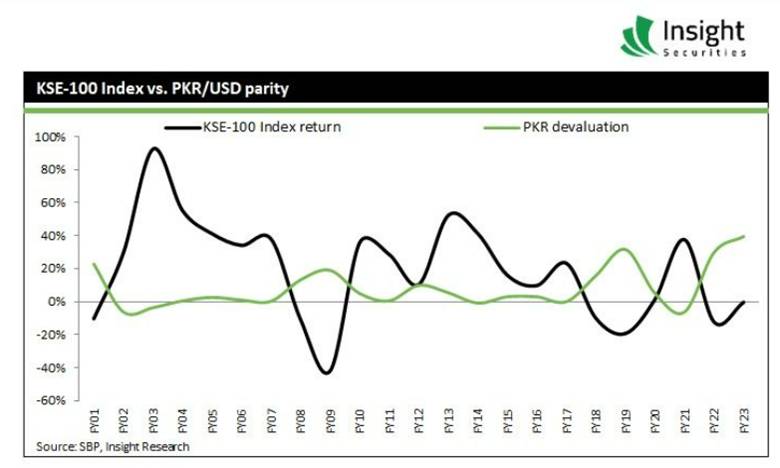

The appreciation has a significant upside in the short run. As per a report by JS Global, “With the expected trend of disinflation to continue, while we expect FY24F average CPI to clock in at 23%, rising oil prices are a key risk to our estimates, which is likely to have a snowball impact on food and related segments that carry ~40% weigh in the basket. Having said that, recent sharp PKR appreciation against US$ is expected to offset some of the POL price hikes announced of late.”

Further, if historical trends are to be relied upon, the stock markets are also likely to experience an extended rally post appreciation.

“In the past 20 days, the domestic currency has rebounded by approximately PKR18 against the USD, primarily due to proactive measures against hoarding and smuggling. We believe that this administrative effort, combined with an expected improvement in remittances resulting from a reduced gap between open and interbank rates, along with essential structural reforms, will contribute to stabilizing the domestic currency. This stabilization could potentially trigger a rally in the local stock market, especially considering that the market is already trading at attractive valuation levels,” remarked, Zubair Ghulam Hussain, CEO at Insight Securities Pvt Limited.

Sustaining the run

However, due to the limited number of active participants in the interbank market and lower trading volumes overall, the lack of depth can pose challenges when trying to buy or sell large amounts of currencies without significantly affecting their exchange rates.

Given the liquidity situation in recent months, it may become more difficult for buyers and sellers to find counterparties willing to trade at their desired prices. Therefore, as the exporters rush to sell their currency in the forward market, there may be a limited supply of currency available for immediate sale in the spot market.

Source: JS Global

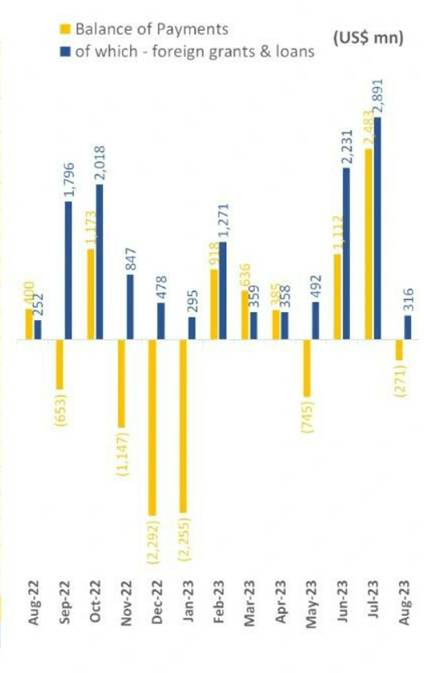

Additionally, Pakistan's foreign exchange reserves remain under significant pressure and require additional inflows to manage upcoming debt payments. The caretaker government is relying on the successful disbursement of the second tranche of the IMF funds, expected after the November review, along with inflows from institutions such as the World Bank and the Asian Development Bank.

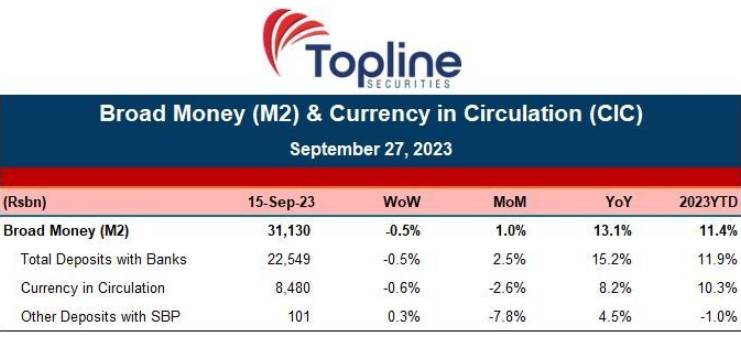

Domestically, there have been positive developments that can alleviate the pressures on the exchange rate. One notable development is the decrease in the broad money supply and currency in circulation.

Source: Topline Securities

Yet, if the government fails to keep tabs on the fiscal imbalance and keeps leveraging financing from the domestic sector, the decrease in money supply might not be sustained.

A nearly $4.5 billion hole has surfaced in Pakistan’s external financing plan and its budget may also overshoot by another Rs1 trillion due to the understatement of debt expenditures, which may become a serious issue during the first review of the International Monetary Fund…

— Shahbaz Rana (@81ShahbazRana) September 20, 2023

What’s Next?

As further corrective measures, including the allowance for commercial banks to establish exchange companies, are being implemented, there is a general consensus among market observers that the trend of depreciation will remerge unless there are significant dollar inflows. Additionally, many have expressed the opinion that the parallel market, although currently curbed, may reemerge as long as there is speculative demand and market players find ways to circumvent restrictions.