There is a sense of prevailing calm among the population regarding Pakistan's economic prospects. After a year and a half of volatility, the country now appears to be on track for recovery. The International Monetary Fund (IMF) review was completed within weeks, the stock market is on the rise, and the Caretaker Prime Minister recently announced the signing of MoUs for projects worth billions.

However, it is unfortunate that much of this is merely a facade to conceal what is brewing beneath the seemingly smooth transition to recovery. The economic fundamentals look bleak, with low growth projections, unemployment rates that continue to persist, and little progress seen in the balance of payment indicators.

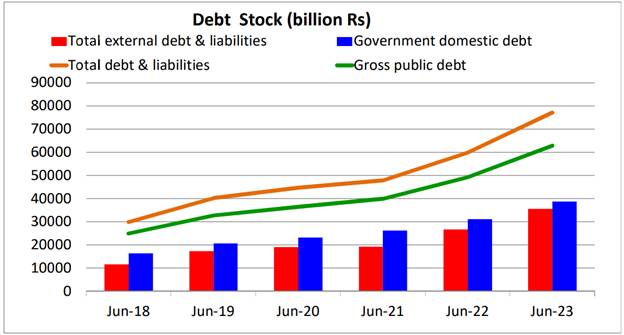

Additionally, the financial managers of the country are also facing sleepless nights due to the most significant challenge in the near-term—public debt sustainability.

Pakistan’s caretaker finance minister (FM), Shamshad Akhtar, in her recent media interactions, reiterated the concerns about the country’s growing debt obligations and the crippling debt servicing cost.

Interest payments on the country's domestic and foreign debt now make up over 90% of all government expenditure. This increase is due to the depreciated rupee and record-high interest rates implemented to combat inflation, resulting in a significant rise in debt servicing costs.

Adding to the pressures are external debt repayments falling due in the second half of the year which amplifies the rollover risk.

According to an analysis note published by JS Global Capital in November, the Governor of the State Bank of Pakistan (SBP) stated, after the recent Monetary Policy Committee (MPC) meeting, that the country's external debt payment obligations total $21 billion for Fiscal Year (FY) 2024.

Of this amount, $4.3 billion has already been paid in the first four months of the fiscal year, leaving approximately $17 billion still outstanding. The SBP anticipates rolling over $12.3 billion, slightly higher than the $11 billion discussed in the previous briefing in September 2023. The remaining $4.4 billion will be paid to the respective lenders.

Coming back to the FM’s statement, she not only acknowledges the unsustainable levels of debt accumulated but also hinted towards possible corrective measures to tackle these challenges.

The Governor of the State Bank of Pakistan (SBP) stated that the country's external debt payment obligations total $21 billion for Fiscal Year (FY) 2024.

Domestic borrowing constitutes the largest portion of total public debt and hence has the highest servicing cost. The government’s massive appetite for deficit financing through short term domestic borrowing has led to a dual crisis of high interest costs and short maturity terms.

Mustafa Pasha, Chief Investment Officer at Lakson Investments, elaborates on the issue, “In the last few months, the government has been strategically focused on borrowing through T-bills and floating PIBs. However, both options have led to high servicing costs due to the prevailing inverted yield curve over the past year. Additionally, relying on T-bill borrowings has increased rollover risk because of their short maturity terms. To address this issue, it appears that the government is now shifting towards issuing higher maturity bonds, which is being facilitated by favorable bids from market participants who anticipate upcoming interest rate cuts.”

Extending maturity terms is also a recurring policy directive from the IMF. “Going forward, with the resumption of appropriate macro policy settings, it will be key to lengthen the maturity profile of public debt as well as managing the cost-risk trade-off of fixed-rate versus floating-rate long-dated debt. Relatedly, work with international partners to develop the local bond market would be helpful to address Pakistan’s debt management challenges,” read the IMF Standby Agreement (SBA) signed in June.

As explained, a shift towards maturity extension is already happening, the second part of the IMF requirement pertaining to development of local bond markets is where the government is planning its next move.

Pakistan's external obligations amount to over $120 billion, and when combined with interest costs, Pakistan is projected to pay over $60 billion in the upcoming three years.

The FM highlighted the government’s intention to tap into market depth by listing debt securities on the stock market, hence raising additional amounts at lower rates.

“The proposed move aims to broaden participation in the government bond market beyond banks, enabling corporations and individuals to directly invest in government debt. This shift would provide an alternative option for the government to raise funds. Currently, only banks are eligible to bid for government securities, so allowing additional players would enhance market depth. Whether or not the impact will be substantial remains to be seen,” remarked Yousuf Farooq, Director Research at Chase Securities.

However, Pasha remains skeptical of this move. “Previous attempts to list government securities have had limited success, but the idea itself is promising. To effectively promote these instruments, a substantial awareness campaign is necessary, and this could serve as a great starting point. However, it is crucial for the government to streamline the trading process to ensure that the market is easily accessible and liquid at par with other securities.”

This brings us to the other aspect of the debt problem, which is the country's external obligations. Pakistan's external obligations amount to over $120 billion, and when combined with interest costs, Pakistan is projected to pay over $60 billion in the upcoming three years.

As per Bloomberg, “Pakistan’s high debt payments and an external funding gap are weighing on the rupee. The country was on the brink of a default this year, and falling investments from overseas and Asia’s fastest inflation are adding to its woes. Remittances also stay muted, making it more dependent on foreign aid for dollar flows.”

Source: SBP

According to the analysis by Topline Securities, “Considering Pakistan external debt repayment of $64 billion for next 3 years as per IMF, another IMF loan will be needed after the completion of this short term facility. We expect that new government will negotiate a 3–4 year loan program worth $8-10 billion. The new IMF deal may include the much-needed Debt Reprofiling or Debt Restructuring along with new taxes on real estate, retail/whole sector, export sector, wealth, gift, inheritance etc as seen in case of Sri Lanka.”

However, considering Pakistan’s debt composition, restructuring remains a challenging task for any administration.

The country finds itself with limited options to manage the crisis, leaving little room for maneuverability. It appears that enforced austerity measures will continue, without any restructuring of domestic debt, while the banking sector may face elevated taxation.

As per the Finance Minister, majority of Pakistan's external debt, 44%, is held by multilateral agencies and cannot be reprofiled due to their “preferred creditor” status. Commercial debt makes up 14% of the external debt, and restructuring this portion is challenging due to the involvement of numerous stakeholders and a cumbersome process. Bilateral debt represents 35% of the external debt, and the government has already benefited from the payment moratorium G-20 debt relief initiative following the COVID-19 pandemic.

Further, any debt negotiations would require China’s stamp of approval to which the country owes around 30% of external public debt. This condition in itself is a non-starter.

China is already struggling with its domestic financial crisis and agreeing on taking haircuts on foreign lending could exacerbate the problem. Additionally, it has ongoing negotiations with multiple countries therefore Chinese would avoid setting a precedent that would lead to similar demand from other bilateral partners. The likely way for them to facilitate Pakistan is through rolling over debt payments that fall due in the near-term.

As per Yousuf Farooq, “Debt relief is unlikely and should not be expected. The only way forward is doing small, consistent current account surpluses and keeping the currency at levels where exports grow.”

The country finds itself with limited options to manage the crisis, leaving little room for maneuverability. It appears that enforced austerity measures will continue, without any restructuring of domestic debt, while the banking sector may face elevated taxation. On the external front, tight liquidity is expected due to the absence of significant debt relief, potentially leading to further depreciation of the rupee. Inflation, while decreasing due to the high base effect of the previous fiscal year, is still expected to remain relatively high.

As all this transpires, it is essential to acknowledge that the country's democratic system remains suspended, with elections yet to take place. Further, the security situation in the country is deteriorating as the government finds it difficult to put a leash on the Taliban. Meanwhile, the administration, has been busy scapegoating Afghan refugees, and neglecting the plight of the country's poor who bear the disproportionate burden of the ongoing cost of living crisis. This situation is a result of the lack of policy direction for years and by the looks of it, there are no quick fixes to it.