The Pakistan Stock Exchange (PSX) has recently witnessed an extended rally following the IMF deal, with the benchmark KSE-100 index registering a gain of 13.6% in July alone. This upward trend is expected to continue if external pressures are further alleviated through the injection of additional funds, particularly through asset sales and Foreign Direct Investment (FDI) from the Gulf countries.

Read more: After IMF Deal, Pakistan Looks to Foreign Direct Investment For Economic Lifeline

However, it is important to note that the recent performance of the PSX does not provide a comprehensive picture in terms of stock performance. Further, there are potential risks, such as increasing political uncertainties and a potentially misguided monetary policy, which could pose significant challenges for those invested in Pakistani equities.

Decoding the PSX Rally

The KSE-100 index is essentially a total return index, meaning that its value is derived from not only the stock prices, but also the income generated by the stocks, particularly dividends.

“KSE-100 is a total return index and incorporates dividends - as a result 47,000 does not correspond to stock prices having recovered to November 2021 levels. KSE-100 market cap is 17% lower than November 2021 - also partially reflected in 'price index' (KSE-30) trending 8% lower vs November 2021,” read a report by JS Global.

Source: JS Global

The argument holds true as the overall market profitability has surged recently primarily driven by three sectors; Oil & Gas Exploration (E&Ps), Banks and Oil Marketing Companies (OMCs).

https://twitter.com/InvestKaar/status/1685519441755275264

However, as per the JS report, “The comparison is even more stark on a Price/Earning (P/E) basis where due to consistent corporate profitability growth not being reflected in stock prices, P/E multiples are currently hovering around 3x vs 5.5x in November 21.”

Source: JS Global

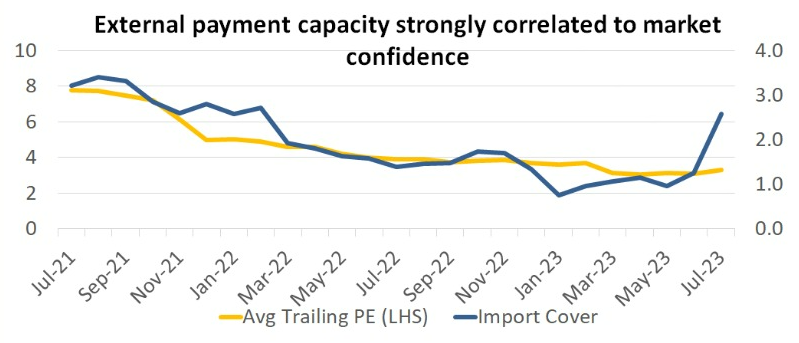

Further, there exists a significant correlation between the country's benchmark index and its liquidity situation. Import cover, which serves as an indicator of this correlation, has recently recovered to the levels observed in November 2021 due to inflows from the IMF and friendly countries. However, the price-to-earnings (P/E) ratio has not yet fully reflected this improvement.

Source: Tellimer

Monetary tightening

The IMF, in its recent Standby Agreement (SBA) review report, states that Pakistan is expected to experience a decrease in headline inflation. This is mainly due to the base effects of the previous year’s rise in fuel and electricity prices, as well as a decline in the global price of food items. However, it is projected that price pressures will remain high, partly due to the delayed monetary tightening by the State Bank of Pakistan (SBP). As a result, the average headline inflation is expected to stay above 25 percent in FY24.

Additionally, following the guidelines set forth by the IMF, the Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) is scheduled to meet on Monday, July 31st. It is anticipated that the committee will consider raising interest rates to keep a tab on inflation.

Regarding the impact on stock prices, Amreen Soorani, Head of Research at JS Global, commented, "It seems that the market has already priced in the potential interest rate hike, given its alignment with the IMF's recommendation to maintain tightened policies. Consequently, the market may not necessarily respond negatively to such an increase."

Furthermore, Mustafa Pasha, Chief Investment Officer at Lakson Investments, expressed a different point of view, stating, "Market expectations are somewhat divided, so a 100 basis points (1%) hike could initially trigger a knee-jerk reaction. However, if there is positive news regarding USD flow and the transition to a caretaker government, any negative impact is likely to be temporary."

Political and security risks

Journalist Khurram Husain, in his article for Dawn, argues that the fragmented implementation of the IMF program by three different governments raises concerns and poses ownership problems. The stakes are high, as failure to successfully complete the program could potentially lead to debt restructuring. Considering this, there is a possibility that the establishment might consider an extended caretaker setup for the smooth implementation of the program. However, it is important to note that such an arrangement could potentially hinder the reconstitution of democracy.

Additionally, after the Afghan Taliban's resurgence in Afghanistan, Pakistan has experienced a significant increase in insecurity and terrorist incidents. The country is witnessing a rise in acts of terrorism, leading to an escalating number of casualties. The border region of Balochistan and Khyber Pakhtunkhwa provinces has become a primary target for banned groups like the TTP, BLA, and ISKP. This situation also poses a threat to foreign investments in the country, including those from China, which have provided crucial financial support to Pakistan during these challenging times.

https://twitter.com/UzairYounus/status/1685636689308344320?t=yFUIlFbWomW0U0_xq0gH-w&s=09

Therefore, if not alleviated, the combined political and security risks can lead to a liquidity problem. However, some analysts suggest that despite Pakistani securities, particularly international bonds, trading at near default levels, they are still being purchased by investors. This is due to the Pakistani government's historical track record of displaying a clear willingness to pay, irrespective of the liquidity situation, unlike countries like Argentina.

Read more: After IMF Deal, Pakistan Looks to Foreign Direct Investment For Economic Lifeline

However, it is important to note that the recent performance of the PSX does not provide a comprehensive picture in terms of stock performance. Further, there are potential risks, such as increasing political uncertainties and a potentially misguided monetary policy, which could pose significant challenges for those invested in Pakistani equities.

Decoding the PSX Rally

The KSE-100 index is essentially a total return index, meaning that its value is derived from not only the stock prices, but also the income generated by the stocks, particularly dividends.

“KSE-100 is a total return index and incorporates dividends - as a result 47,000 does not correspond to stock prices having recovered to November 2021 levels. KSE-100 market cap is 17% lower than November 2021 - also partially reflected in 'price index' (KSE-30) trending 8% lower vs November 2021,” read a report by JS Global.

Source: JS Global

The argument holds true as the overall market profitability has surged recently primarily driven by three sectors; Oil & Gas Exploration (E&Ps), Banks and Oil Marketing Companies (OMCs).

https://twitter.com/InvestKaar/status/1685519441755275264

However, as per the JS report, “The comparison is even more stark on a Price/Earning (P/E) basis where due to consistent corporate profitability growth not being reflected in stock prices, P/E multiples are currently hovering around 3x vs 5.5x in November 21.”

Source: JS Global

Further, there exists a significant correlation between the country's benchmark index and its liquidity situation. Import cover, which serves as an indicator of this correlation, has recently recovered to the levels observed in November 2021 due to inflows from the IMF and friendly countries. However, the price-to-earnings (P/E) ratio has not yet fully reflected this improvement.

Source: Tellimer

{kind=link}

Monetary tightening

The IMF, in its recent Standby Agreement (SBA) review report, states that Pakistan is expected to experience a decrease in headline inflation. This is mainly due to the base effects of the previous year’s rise in fuel and electricity prices, as well as a decline in the global price of food items. However, it is projected that price pressures will remain high, partly due to the delayed monetary tightening by the State Bank of Pakistan (SBP). As a result, the average headline inflation is expected to stay above 25 percent in FY24.

Additionally, following the guidelines set forth by the IMF, the Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) is scheduled to meet on Monday, July 31st. It is anticipated that the committee will consider raising interest rates to keep a tab on inflation.

Regarding the impact on stock prices, Amreen Soorani, Head of Research at JS Global, commented, "It seems that the market has already priced in the potential interest rate hike, given its alignment with the IMF's recommendation to maintain tightened policies. Consequently, the market may not necessarily respond negatively to such an increase."

Furthermore, Mustafa Pasha, Chief Investment Officer at Lakson Investments, expressed a different point of view, stating, "Market expectations are somewhat divided, so a 100 basis points (1%) hike could initially trigger a knee-jerk reaction. However, if there is positive news regarding USD flow and the transition to a caretaker government, any negative impact is likely to be temporary."

Political and security risks

Journalist Khurram Husain, in his article for Dawn, argues that the fragmented implementation of the IMF program by three different governments raises concerns and poses ownership problems. The stakes are high, as failure to successfully complete the program could potentially lead to debt restructuring. Considering this, there is a possibility that the establishment might consider an extended caretaker setup for the smooth implementation of the program. However, it is important to note that such an arrangement could potentially hinder the reconstitution of democracy.

Additionally, after the Afghan Taliban's resurgence in Afghanistan, Pakistan has experienced a significant increase in insecurity and terrorist incidents. The country is witnessing a rise in acts of terrorism, leading to an escalating number of casualties. The border region of Balochistan and Khyber Pakhtunkhwa provinces has become a primary target for banned groups like the TTP, BLA, and ISKP. This situation also poses a threat to foreign investments in the country, including those from China, which have provided crucial financial support to Pakistan during these challenging times.

https://twitter.com/UzairYounus/status/1685636689308344320?t=yFUIlFbWomW0U0_xq0gH-w&s=09

Therefore, if not alleviated, the combined political and security risks can lead to a liquidity problem. However, some analysts suggest that despite Pakistani securities, particularly international bonds, trading at near default levels, they are still being purchased by investors. This is due to the Pakistani government's historical track record of displaying a clear willingness to pay, irrespective of the liquidity situation, unlike countries like Argentina.