“With how many things are we on the brink of becoming acquainted, if cowardice or carelessness did not restrain our inquiries.” - Frankenstein, by Mary Shelley

This piece is inspired by a letter to the editor, written by this scribe earlier and published in Dawn. After the publication of the letter, an overwhelming sense of comradery was witnessed — the unaffected faction of CA students remained valiantly vocal alongside the repressed group. Subsequently, another letter was later published in the same newspaper – a response from the subject of critique.

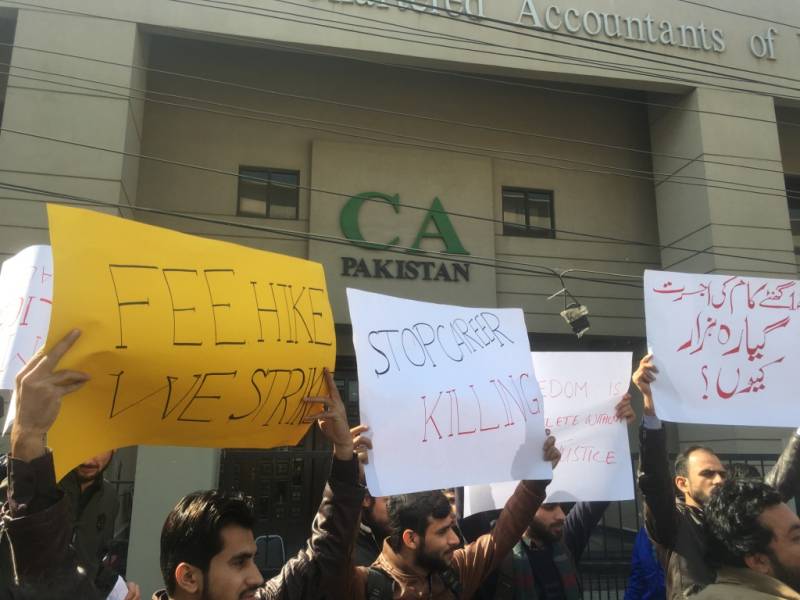

Firstly, rendering a preamble to whoever is not intimate with the specie under observation. The Institute of Chartered Accountants of Pakistan (ICAP) was established under an ordinance in 1961, and is a regulatory body mandated with the task of regulating the accountancy profession. This includes awarding the qualification of Chartered Accountancy and overseeing membership. ICAP has a council responsible for formulating policies in the interest of the profession and the public.

The dialectical currents underlying it are discernible from the fact that the Council, which is meant to formulate policies and frameworks, are themselves partners of the training organizations and firms at the behest of the Council. In other words, they regulate themselves.

The Council consists of 19 members, of which 15 are elected by members i.e. fellow qualified CAs, and 4 are nominated by the government. These nominations, which include —apparently the most ideal and readily available individuals for such a responsibility — the Chairman FBR, Chairman SBP, Governor SBP, and Finance Minister, are seemingly present to lend an independent viewpoint in the day-to-day affairs of the echelon. However, their non-existent attendance, as reported in the Annual Report 2023 published by the Institute, raises questions about their resolve and commitment.

Unlike the HEC, which is seemingly an exclusive educational thermostat, ICAP partakes in a high-handed role as a market operator, alongside its denominational pedagogical role. The dialectical currents underlying it are discernible from the fact that the Council, which is meant to formulate policies and frameworks, are themselves partners of the training organizations and firms at the behest of the Council. In other words, they regulate themselves, including crucial policy matters such as the fixation of stipends, which as of now, is around twenty-thousand rupees monthly at the commencement of training — not even close to the minimum wage, let alone a considerable return on tedious value-addition.

Whenever this totalitarian stipend policy is canvassed, the protégés of the junta and outright simpletons contend that the “stipend” should not be equated with a wage or salary; the former is akin to pocket money for covering day-to-day expenses of a student: the efficacy of this amount even in fulfilling the supposed purpose, given the staggering level of inflation and fallout poverty, should not be a surprise.

The absurdity of this contention transcends my rather limited intelligence - how can one even strive to vindicate this ostensible conflict of interest and the surplus value being ruthlessly extracted from trainees, mostly belonging to the middle and lower-middle class, by the stalwarts of accountancy, over the pretext of “learning.” If one is earning a hefty amount of cash from the value derived from someone's labor, then the laborer has an unequivocal right to a proportion of those earnings concurrently.

Perhaps, it is nothing but an archetypical capitalist oligarchy, wherein the exploiters themselves are in the position of delivering justice to the exploited and hence, sardonically, the accountability function proliferates the hegemony of discontent over the beleaguered subjects. This overt conflict of interest has been a precursor of ordeal unto students belonging to the middle and lower-middle class.

Amidst this prevailing gross disparity, recently, the ICAP ordained the disenfranchisement of students from getting registered, save extraordinary hardships, with a training organization if they do not apply within 6 months of the CAF, after which one is required to embark on their mandatory training. Whenever this policy is probed, a frequent response is that this is a utopian - radically countering the "exploitation" being meted out by training organizations while inducting trainees, by not registering them as a trainee and hence, savoring free labor in the place of undervalued work. To this, I have a rebuttal: if the Council is so heavenly concerned apropos the prevailing atrocities imparted unto students, how many firms have been blacklisted till today due to inappropriate treatment meted out to students?

Either cynicism appears to be a commonplace feat among these regulators, or due to the radical encumbrance of delivering exquisite performance, the Council has overlooked the need to align its core values with reality.

Another viewpoint being coopted in the digital battlefield is that students don't choose not-so-pristine firms and end up wasting their precious time. This line of argumentation seems blatantly illogical to me, as it should be an individual’s discretion where to work or where not to, and even if someone is willing to wait for a more prestigious opportunity, how it will ultimately alter the demand-supply continuum at the larger level is unclear. Mere reading of this benevolence would enlighten the couched patronage: squandering ingenious labor, which otherwise would cost at least six digits, to substandard firms associated with the Council.

Moreover, in the letter mentioned, ICAP flaunted that 95% of the CAF-qualified students in Spring 2023 were inducted into a training organization as of now, without stating the perennial anxiety that grips young minds, and the coercive inductions into hostile workplaces.

Notwithstanding the foregoing, ironically, ICAP’s core value, as stated on their website, includes 'equity’ and ‘fairness,’ that is, “there is unanimity of the view at the Institute that merit and merit alone would remain the criteria for decision making at all levels and spheres. In ICAP, every stakeholder’s views are heard and respected and there is zero tolerance for disrespect, harassment and injustice.”

Either cynicism appears to be a commonplace feat among these regulators, or due to the radical encumbrance of delivering exquisite performance, the Council has overlooked the need to align its core values with reality.