A recent Staff Report by the International Monetary Fund (IMF) has highlighted the significant economic challenges facing Pakistan. These challenges are the result of a combination of factors, including a political crisis, last year's floods, tightening external financing conditions, and adverse domestic policies. According to the report, the economy has been experiencing a slowdown, as key indicators reflect the severity of the situation.

A major concern mentioned in the report is the decline in international reserves, which stood at around three-fourths of a month of import cover, equivalent to $4.2 billion at the time of the review. Inflation has also reached a peak of 38% in May 2023, which poses a risk to debt sustainability alongside fiscal pressures.

The report also emphasized on growing social discontent among the population, particularly evident in the escalating political tensions in May. These tensions, as per the Fund, have exposed underlying fractures within the political and institutional landscape of the country.

https://twitter.com/UzairYounus/status/1681326385799868417

The magnitude of the crisis

According to the review, consumer and business confidence have significantly weakened due to economic and political uncertainties, leading to speculations about the possibility of a sovereign debt default. Despite some informal measures, external pressures have intensified, resulting in a shortage of dollars and disruptions in import-dependent sectors.

https://twitter.com/ShahidAliHabib1/status/1681334776614076416

The Fund attributed the rising inflation to increasing food prices and the impact of depreciation. It also pointed out that the lack of clarity from the State Bank of Pakistan (SBP) in determining the appropriate monetary stance has further aggravated the situation.

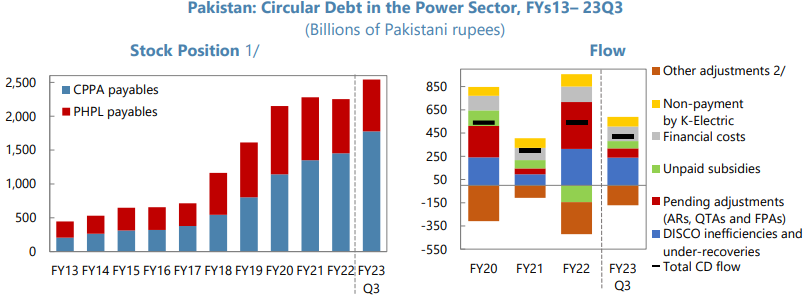

On the fiscal side, challenges have emerged from pressures on revenue collection, particularly from the petroleum development levy (PDL) and sales tax on imported goods. Additionally, unbudgeted expenditures on energy subsidies and relief measures have contributed to increased spending. The power sector, in a dismal state, has also contributed to the challenges, with circular debt reaching a record of Rs. 2.5 trillion.

Source: IMF

The report also addresses Pakistan's previous program, which came to an incomplete end in June. Although it initially played a role in stabilizing the economy and providing crucial support during the pandemic, there were recurring deviations from the program, happening ironically shortly after successful reviews. The challenges posed by the disastrous events of 2022 made it unachievable to reach the original program goals, thus necessitating a new agreement.

Outlook

Looking ahead, the IMF recognizes the uphill battle that Pakistan faces. Gross financing needs have increased, while external market financing has become scarce, resulting in weak investor confidence. Credit rating agencies have downgraded Pakistan to a rating just above default, highlighting the importance of multilateral and official bilateral support in meeting debt obligations.

The IMF has projected moderate growth of approximately 2.5 percent in fiscal year 2024. While the recovery from the floods is expected to have a positive impact, it will take time for the easing of import restrictions to make a noticeable difference. External challenges and the need for strict macroeconomic policies will limit the extent of the recovery. Additionally, the IMF anticipates headline inflation to remain above 25% on average in fiscal year 2024.

https://twitter.com/sohailkarachi/status/1681328578221203458

It is expected that the State Bank of Pakistan (SBP) will continue with its tightening cycle in order to restore consumer confidence and manage inflation expectations. The IMF has also advised the government to maintain a ±1.25 percent range on average for the interbank-open market premium, ensuring a free exchange rate.

A major concern mentioned in the report is the decline in international reserves, which stood at around three-fourths of a month of import cover, equivalent to $4.2 billion at the time of the review. Inflation has also reached a peak of 38% in May 2023, which poses a risk to debt sustainability alongside fiscal pressures.

The report also emphasized on growing social discontent among the population, particularly evident in the escalating political tensions in May. These tensions, as per the Fund, have exposed underlying fractures within the political and institutional landscape of the country.

https://twitter.com/UzairYounus/status/1681326385799868417

The magnitude of the crisis

According to the review, consumer and business confidence have significantly weakened due to economic and political uncertainties, leading to speculations about the possibility of a sovereign debt default. Despite some informal measures, external pressures have intensified, resulting in a shortage of dollars and disruptions in import-dependent sectors.

https://twitter.com/ShahidAliHabib1/status/1681334776614076416

The Fund attributed the rising inflation to increasing food prices and the impact of depreciation. It also pointed out that the lack of clarity from the State Bank of Pakistan (SBP) in determining the appropriate monetary stance has further aggravated the situation.

On the fiscal side, challenges have emerged from pressures on revenue collection, particularly from the petroleum development levy (PDL) and sales tax on imported goods. Additionally, unbudgeted expenditures on energy subsidies and relief measures have contributed to increased spending. The power sector, in a dismal state, has also contributed to the challenges, with circular debt reaching a record of Rs. 2.5 trillion.

Source: IMF

The report also addresses Pakistan's previous program, which came to an incomplete end in June. Although it initially played a role in stabilizing the economy and providing crucial support during the pandemic, there were recurring deviations from the program, happening ironically shortly after successful reviews. The challenges posed by the disastrous events of 2022 made it unachievable to reach the original program goals, thus necessitating a new agreement.

Outlook

Looking ahead, the IMF recognizes the uphill battle that Pakistan faces. Gross financing needs have increased, while external market financing has become scarce, resulting in weak investor confidence. Credit rating agencies have downgraded Pakistan to a rating just above default, highlighting the importance of multilateral and official bilateral support in meeting debt obligations.

The IMF has projected moderate growth of approximately 2.5 percent in fiscal year 2024. While the recovery from the floods is expected to have a positive impact, it will take time for the easing of import restrictions to make a noticeable difference. External challenges and the need for strict macroeconomic policies will limit the extent of the recovery. Additionally, the IMF anticipates headline inflation to remain above 25% on average in fiscal year 2024.

https://twitter.com/sohailkarachi/status/1681328578221203458

It is expected that the State Bank of Pakistan (SBP) will continue with its tightening cycle in order to restore consumer confidence and manage inflation expectations. The IMF has also advised the government to maintain a ±1.25 percent range on average for the interbank-open market premium, ensuring a free exchange rate.