China, the leading bilateral lender of the developing world, is apparently paying a massive cost to safeguard its Belt and Road Infrastructure (BRI) projects.

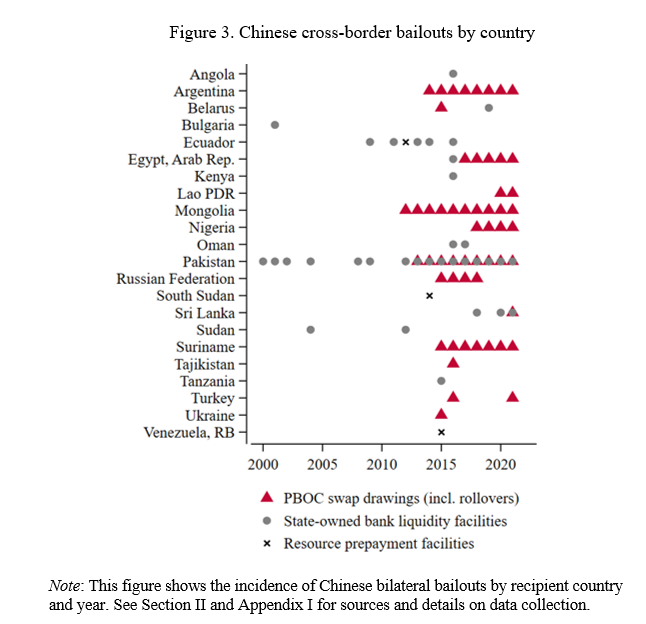

According to a new paper published on China's role in global finance, the country has spent $240 billion between 2008 and 2021 on bailing out 22 developing countries.

Amongst the top recipients were Argentina, Pakistan and Egypt with $111.8 billion, $48.5 billion and $15.6 billion in bailouts respectively.

Source: Horn et al.

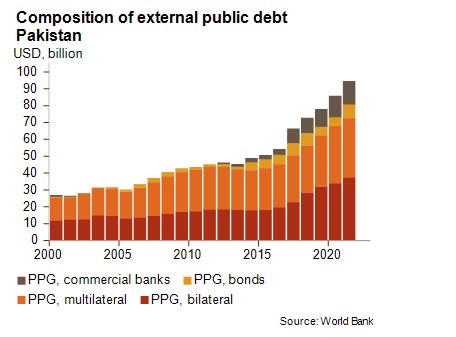

Pakistan has been at the forefront of BRI through China’s flagship project, CPEC. Former Finance Minister Miftah Ismail stated that Pakistan owes around $30 billion, which constitutes approximately 30% of its foreign debt, to China. This amount can be broken down into $4 billion in deposits with the SBP, $5-6 billion in loans from Chinese state-owned commercial banks, and roughly $20 billion in project loans (mostly CPEC related) owed to China.

Many around the globe are skeptical about debt from China due to stringent clauses attached to it. Among these are a few prominent ones including: cross-default, which allows Chinese lending authorities a right to demand immediate repayment in case a country default on any other loan repayment (e.g. World Bank), and a stabilisation clause that prevents a country to apply new laws to Chinese financed projects, along with a clause that restricts borrowing country to compel China from agreeing to terms similar to what has been agreed on with other creditors like the Paris Club.

Further, the interest rates attached to Chinese loans are usually higher than those imposed by other bilateral lenders or the IMF and World Bank.

Yet, given Pakistan’s precariousfinancial condition, it needs Chinese assistance more than ever before. “Even if Islamabad is actively exploiting all available options to buy time, Pakistan is on verge of a sovereign debt default. Its public finances are extremely weak, with public debt (77.8% of GDP) having reached nearly 650% of government revenues in FY22. Its interest payments culminating at around 40% of government revenues (the world’s third highest level after Sri Lanka and Ghana),” tweeted economist Muneeb Sikander.

Coming back to the study, it highlighted that a key tool deployed by China for rescuing debt distress nations was Central Bank swaps. What are these?

Central bank currency swaps involve two central banks agreeing to exchange their respective currencies for a defined period. The intention behind these agreements is to enable central banks to provide their currency to other central banks in situations of financial pressure or scarcity of a particular currency. The aim is to ensure that financial institutions have sufficient access to liquidity to avoid financial instability and maintain operations.

“Countries with (i) low liquidity levels and (ii) low ratings are those drawing most from the the People’s Bank of China (PBOC) (thus bolstering their gross reserves), showing that countries prop up reserves to avoid rollover crisis & default,” Christoph Trebesch one of the authors of the paper tweeted.

“PBOC swap lines have become an important tool of China’s overseas crisis management. In total USD 170 billion of swaps have been extended (in RMB). This includes repeated rollovers (de facto maturity is 3 years, a very different animal than the Fed’s short swaps),” he added further.

Another key component of China’s rescue financing identified in the report were bilateral loans, which involve balance of payment assistance from Chinese state-owned banks amounting to over $70 billion. As per the findings, the quantum of Chinese bailouts was around 20% of the IMF’s total lending over the last decade.

“In the past, Beijing has tended to lend more money to some countries, including Argentina, Ecuador and Pakistan, so that they can continue to make payments on existing loans. China’s approach helps these countries afford imports of food and fuel, but leaves them with ever more debt,” reads an article in The New York Times.

Nonetheless, countries such as Pakistan are mostly responsible for their present debt situation due to the prolonged existence of structural disparities, which are now haunting them.

Miftah Ismail touched upon the issue in a session with Brookings Institution stating, “The power plants being built, or roads and highways being constructed (under CPEC) aren’t generating enough dollars (to repay loans) and neither are they improving productivity by that much.”

Economist Atif Mian, on the Brookings panel with Miftah, shared the same views, “If you can’t payback the loans then it means that you aren’t growing, and the projects haven’t been that beneficial.”

Therefore, the challenge for developing countries like Pakistan is very clear, they need to be able to find a balance between development initiatives and managing their overall debt.